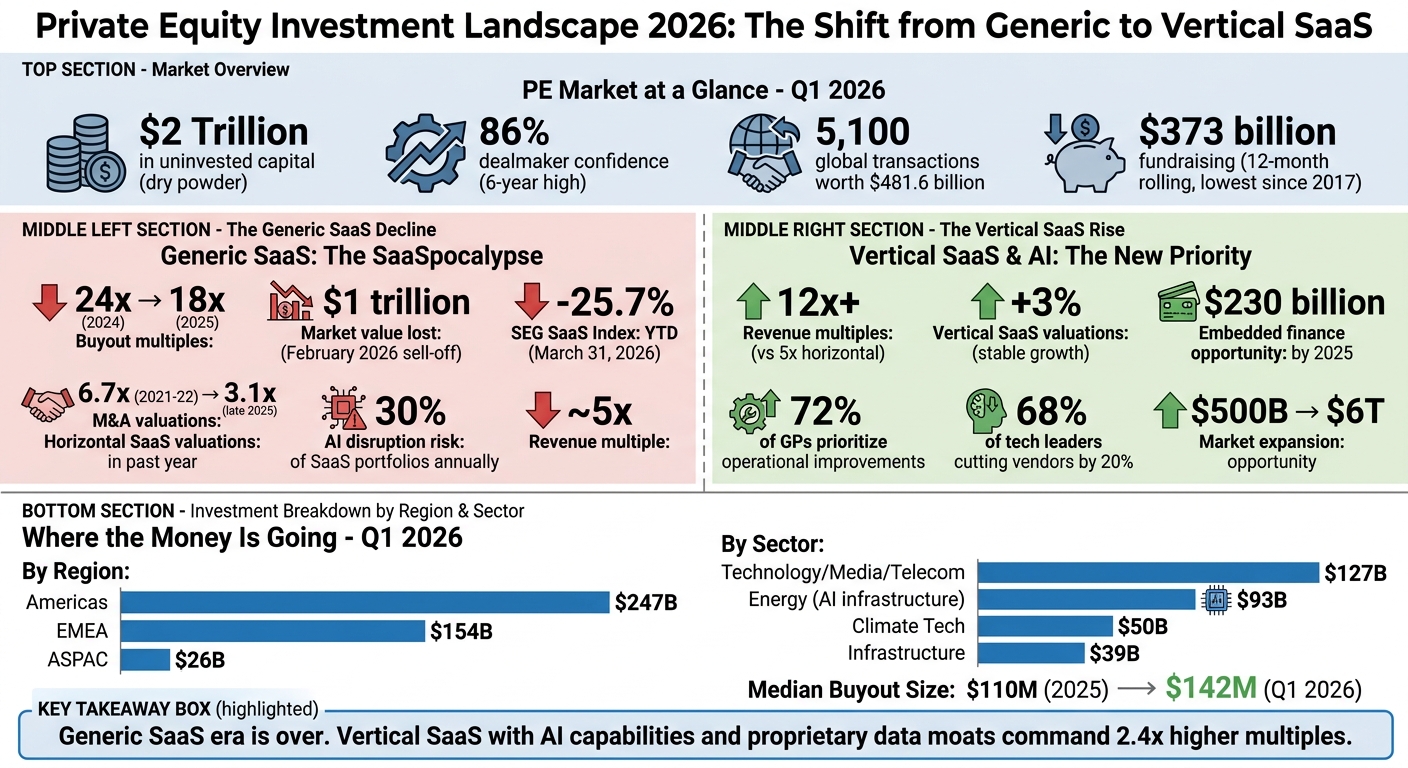

Private equity (PE) firms are sitting on $2 trillion in uninvested capital as of 2026, with confidence in the market at its highest in six years. However, none of this money is flowing toward generic SaaS companies. Instead, PE firms are targeting AI-driven tools and vertical SaaS platforms that focus on industry-specific solutions. Here’s why:

- Generic SaaS struggles: Slowing growth, declining buyout multiples (from 24x in 2024 to 18x in 2025), and competition from AI-native tools are hurting the sector.

- AI disruption: AI agents are replacing traditional software, reducing demand for per-seat licensing models.

- Vertical SaaS appeal: Industry-specific platforms with deep integration and proprietary data are commanding higher revenue multiples (12x+ vs. 5x for horizontal SaaS).

- Shift in PE strategy: 72% of General Partners now prioritize value creation through revenue growth and operational improvements, not financial engineering.

PE firms are also investing heavily in AI infrastructure and tools that enhance portfolio efficiency. To attract investment, SaaS companies must focus on specialized, mission-critical solutions with embedded AI capabilities.

Key takeaway: The era of generic SaaS dominance is over. Vertical SaaS and AI-driven platforms are the new priorities for PE investment.

Private Equity Investment Shift: Generic SaaS vs Vertical SaaS in 2026

The Private Equity Market in 2026: Key Data

Deal Activity and Investment Volumes

The private equity (PE) market in Q1 2026 shows some interesting shifts in how investments are being made. Globally, 5,100 transactions were completed, amounting to a total value of $481.6 billion [14]. While these large-scale deals boosted the overall value, the number of transactions reached its lowest point in years [10][12]. This trend highlights what experts are calling a "value-volume dichotomy", where PE firms are becoming more selective. Instead of spreading investments across smaller opportunities, they’re focusing heavily on acquiring "must-own" strategic assets.

Breaking it down by region, the Americas led the charge with $247 billion in deals. The EMA region (Europe, Middle East, and Africa) followed with $154 billion, while the ASPAC (Asia-Pacific) region trailed significantly at $26 billion [12]. Looking at sector trends, Technology, Media, and Telecom (TMT) dominated with $127 billion in investments. However, energy deals surged to $93 billion, driven by the race to develop infrastructure for AI data centers [10]. Climate tech also drew attention with $50 billion in investments, and traditional infrastructure saw $39 billion [10].

The median buyout size climbed to $142 million in Q1 2026, a sharp increase from $110 million in 2025 [10]. This growth reflects a preference for larger, more stable companies with strong cash flows. Donald Zambarano, U.S. Head of Private Equity at KPMG, commented:

"Infrastructure is increasingly becoming the new mega-buyout category, with assets linked to energy, digital infrastructure and data centers attracting the deepest pools of capital" [10].

These figures paint a picture of a market prioritizing quality over quantity, setting the tone for the challenges and strategies in fundraising and exits.

Fundraising and Exit Metrics

Fundraising remains a tough spot for the PE market. In Q1 2026, global fundraising dropped to just $86 billion [14]. Over a rolling 12-month period, totals fell to $373 billion, marking the lowest levels since Q1 2017 [10][12]. This slowdown is largely due to a liquidity bottleneck, as limited partners (LPs) hesitate to commit to new funds while waiting for distributions from older ones. This creates a cycle that’s proving hard to break.

On the exit front, activity has stabilized but remains modest. Q1 2026 recorded 975 exit transactions with a total value of $306.7 billion [14]. However, on a rolling 12-month basis, exit volumes hit a five-year low with just 3,211 deals [10][12]. PE firms are holding onto assets longer, with the average holding period now stretching to about seven years, compared to the historical norm of five to six years [13]. This longer timeline reflects firms’ strategy of waiting for better market conditions rather than settling for lower valuations.

Interestingly, companies exiting through IPOs are in better financial health. In 2025, 64% of IPOs were profitable (positive EBITDA), a significant improvement from 32% in 2019 [11]. This suggests that PE firms are focusing on operational improvements and building stronger businesses before taking them public.

sbb-itb-9cd970b

Ep. 123: Bob Morse, Strattam Capital | Embedding AI into Vertical Software to Drive Portfolio Growth

Why Generic SaaS Is Missing Out on PE's $2 Trillion

Private equity (PE) firms, sitting on a staggering $2 trillion in uninvested capital, are shifting their focus toward specialized, AI-powered tools. This move signals a departure from traditional SaaS platforms that lack differentiation and operational depth.

The SaaSpocalypse: Risks Facing Generic SaaS

The SaaS industry is facing what some are calling a "SaaSpocalypse", as AI agents begin to replace human-operated workflows. The numbers paint a grim picture. In February 2026, a massive investor sell-off wiped out $1 trillion in market value from software and services stocks [17].

AI automation is expected to disrupt 30% of SaaS portfolio companies annually by 2026 [16]. Satya Nadella, CEO of Microsoft, summed it up bluntly:

"SaaS applications will 'collapse' in the agent era, once AI agents take over the business logic layer" [4].

Generic SaaS platforms are increasingly venturing into "dead zones", where AI agents can perform tasks faster and cheaper than traditional software. This shift is creating significant financial risk. Around $100 billion in private credit portfolios are tied to software companies, making up 20% of total business development company (BDC) holdings [4]. In early 2026, concerns over AI disruption led investors to attempt withdrawing more than $10 billion from private credit funds [4]. Apollo Global Management responded by halving its software exposure in direct lending funds from 20% in early 2025 to just 10% by the end of the year [5]. As John Zito, Partner and Deputy CIO at Apollo, put it:

"The real risk is - is software dead?" [5].

Adding to the pressure, the traditional per-seat pricing model is crumbling. AI agents, capable of handling the workload of multiple employees, are reducing the need for individual licenses [17]. Abdul Abdirahman from F-Prime highlighted this shift:

"This may be the first time in history that the terminal value of software is being fundamentally questioned, materially reshaping how SaaS companies are underwritten going forward" [17].

The fallout is evident in the declining valuations of SaaS firms. Average private equity buyout multiples for SaaS companies dropped from 24x in 2024 to 18x in 2025 [5]. Beyond AI-driven devaluation, these companies also face market saturation, further eroding their competitive edge.

Market Saturation and Limited Differentiation

The rise of AI coding agents is making it easier for businesses to create custom software, shifting the "build versus buy" decision firmly toward "build." Many companies are choosing to develop their own tools instead of renewing costly SaaS contracts [17]. One example: in late 2024, Klarna abandoned Salesforce's CRM product in favor of its own AI-driven system, signaling a broader trend in enterprise software purchasing [17].

Generic tools like standard CRM systems and project management platforms are increasingly seen as outdated. AI agents can now handle these tasks directly [6][3]. Igor Ryabenkiy, Founder and Managing Partner at AltaIR Capital, explained:

"If your differentiation lives mostly in UI [user interface] and automation, that's no longer enough. The barrier to entry has dropped, which makes building a real moat much harder" [6].

Jake Saper, General Partner at Emergence Capital, echoed this sentiment:

"Being the connector used to be a moat. Soon, it'll be a utility" [6].

The market is already reflecting these challenges. The SEG SaaS Index, which tracks over 120 public software companies, fell 25.7% year-to-date as of March 31, 2026 [4]. Software M&A valuations have also plummeted, dropping from a peak of 6.7x EV/Revenue in 2021–2022 to just 3.1x by late 2025 [4].

PE firms are accelerating this shift away from generic SaaS. Major players like Blackstone are replacing costly, horizontal SaaS licenses across their portfolio companies with custom AI tools or joint AI ventures to cut expenses [3]. Isaac Kim, Partner at Lightspeed, captured the sentiment:

"Technology private equity, in its current form, is dead" [5].

Today, PE firms are prioritizing solutions with deep integration and proprietary data advantages, steering clear of thin workflow layers and generic tools [6].

Where PE Money Is Going: AI-Driven Tools and Vertical SaaS

As general-purpose SaaS solutions face slowing momentum, private equity (PE) firms are shifting their focus to specialized tools that tackle specific industry needs. Investments are pouring into AI-driven tools and vertical SaaS platforms, which cater to distinct sectors and offer tailored solutions. These platforms are particularly attractive, commanding 12x+ revenue multiples, compared to around 5x for horizontal SaaS [18].

The Rise of Vertical SaaS and AI Ecosystems

PE firms are increasingly favoring companies that manage entire industry workflows rather than generic productivity tools. A standout example is Haveli Investments, which acquired a controlling stake in Sirion Labs - a contract software provider - in January 2026. The deal valued Sirion Labs at approximately $1 billion [2]. Similarly, Everstone Capital took a majority stake in Wingify, a marketing technology SaaS provider. Wingify later agreed to acquire its Paris-based competitor, AB Tasty, for $150–$200 million in early 2026 [8].

While horizontal SaaS valuations plummeted 35% in the past year, vertical SaaS valuations held steady with a slight 3% increase [20]. This stability stems from their deep integration into industry workflows and access to proprietary data, which horizontal solutions often lack.

Adding to their appeal, embedded finance is creating new revenue opportunities for vertical SaaS platforms. By incorporating features like payments, lending, and insurance directly into their software, these platforms are projected to generate $230 billion in revenue by 2025 [18]. For example, in 2025, Kedaara Capital invested $350 million in Impetus Technologies to advance its AI and cloud data platform [8].

This growing emphasis on vertical SaaS is complemented by PE’s increasing use of AI to improve operational efficiency across their portfolios.

PE's Focus on AI Tools for Operations

AI is becoming a cornerstone for PE firms aiming to enhance operational efficiencies. In fact, 72% of General Partners (GPs) cite operational improvements as their top priority for value creation in 2026 [9].

The impact of AI is evident in success stories like Slash Financial, an AI-native business banking platform. In April 2026, the company hit unicorn status after closing a $100 million Series C round led by Ribbit Capital. Over just 24 months, it scaled its annualized revenue from $10 million to $250 million, thanks to AI agents replacing entire departments [19].

Another example is Factory, an autonomous software engineering platform. Backed by Khosla Ventures, Factory raised $150 million in a Series C round in April 2026, reaching a valuation of $1.5 billion. The platform doubled its revenue every month for six straight months, serving major clients like Nvidia and Adobe [19].

In the same month, Wealth.com secured $65 million in an oversubscribed Series B round to expand its AI-powered estate and tax planning platform. Its proprietary engine, Ester Intelligence, processed over 100,000 estate documents in 2025, driving 664% year-over-year growth in its AI workflows. Wealth.com now supports firms managing more than $15 trillion in assets [19].

AI is also expanding the addressable market for enterprise software. What was once a $500 billion market has grown to a $6 trillion opportunity, targeting labor-intensive sectors like insurance underwriting, logistics dispatch, and healthcare scheduling. PE firms are zeroing in on companies that can replace or accelerate high-cost manual tasks in these specialized areas, leaving general-purpose tools struggling to keep up [20].

How SaaS Companies Can Attract PE Investment

SaaS companies relying on outdated strategies - like prioritizing rapid user growth, flashy interfaces, and basic integrations - must adapt to align with the changing priorities of private equity (PE) firms. With $3.7 trillion in global dry powder and $1 trillion ready for deployment in the U.S., PE investors are becoming increasingly selective about their targets [1].

Shifting from Generic SaaS to Vertical Solutions

To catch the attention of PE firms, SaaS companies need to embed themselves into mission-critical, industry-specific workflows. This approach increases switching costs and creates a proprietary data moat - leveraging industry-specific datasets to train AI models that generic systems can't match. Instead of offering general productivity tools, focus on platforms that manage entire processes, such as healthcare scheduling, construction job costing, or insurance underwriting. These vertical solutions often command 12x+ revenue multiples, compared to roughly 5x for horizontal SaaS [18].

Take the acquisition of Sirion Labs by Haveli Investments in January 2026, for instance. The $1 billion deal wasn't just about contract management software - it was about the underlying AI expertise and proprietary contract data that made the platform defensible [2].

Adding embedded finance to your platform can further boost appeal by creating an additional revenue stream. Integrating payments, lending, or insurance directly into the software can significantly increase average revenue per user (ARPU). This strategy is expected to generate $230 billion in revenue by 2025 [18]. Combining vertical specialization with strong AI capabilities is the next logical step.

Using AI to Improve Operations and Value

Once a SaaS company pivots to vertical solutions, integrating AI becomes essential for operational efficiency and measurable margin gains. PE firms now expect AI to deliver results within 12 to 18 months, moving beyond its use as a marketing buzzword. The focus is shifting to "systems of action" - platforms where AI agents directly perform tasks instead of just aiding human operators. Jake Saper, General Partner at Emergence Capital, explains:

"Pre-Claude, getting humans to do their jobs inside your software was a powerful moat, but if agents are doing the work, who cares about human workflow?" [6].

To reflect the value AI brings, consider adopting consumption-based or outcome-based pricing models rather than traditional seat-based pricing [6].

Common Mistakes to Avoid in SaaS Investment Strategies

To maximize investor appeal, it's crucial to avoid common missteps that can weaken your competitive position. While vertical specialization and AI integration are key, there are pitfalls that can undermine these efforts.

One major mistake is relying on shallow AI integrations - basic interfaces built on existing APIs without deep integration or proprietary data. Igor Ryabenkiy, Founder and Managing Partner at AltaIR Capital, cautions:

"If your differentiation lives mostly in UI and automation, that's no longer enough. The barrier to entry has dropped, which makes building a real moat much harder" [6].

Another misstep is sticking to rigid operational structures when PE firms now prioritize sustainable growth models. The market has moved away from the "growth at all costs" mindset, favoring companies that demonstrate profitability and adhere to the "Rule of 40" - where the growth rate plus profit margin exceeds 40%. In 2025, buyout and growth deals exceeding $500 million rose by 44% compared to 2024, favoring companies with clear paths to EBITDA durability [21].

Finally, don't treat AI as just a marketing layer. While 72% of SaaS M&A targets in 2025 referenced AI capabilities [1], investors can easily spot superficial AI implementations. Use the "replication speed test" to evaluate your competitive moat: if a well-funded AI-native team could replicate your core functionality in 6–9 months, your differentiation may be too weak for a premium exit [15].

Conclusion

Private equity firms are redirecting substantial investments away from generic SaaS toward vertical SaaS and AI-driven platforms that seamlessly integrate into essential workflows. With dealmaker confidence reaching an impressive six-year high of 86% in 2026 [22], the focus has shifted to specialized platforms. Vertical SaaS businesses now command revenue multiples exceeding 12x, while horizontal platforms have seen valuations compress to around 5x [18].

At the heart of this transition is the emphasis on creating durable competitive advantages through proprietary data. Companies that harness unique industry datasets and embed themselves deeply into integrated, error-proof workflows establish switching costs that generic platforms struggle to match. As Holden Spaht, Managing Partner at Thoma Bravo, explains:

"We look to buy businesses built around deep domain expertise, zero-tolerance-for-error workflows and embedded cross-system integration" [7].

Operational efficiency has surpassed the "growth-at-all-costs" mindset as the primary driver of value creation. In fact, 72% of General Partners now rank operational improvements as their top priority for 2026 [9]. This trend favors businesses that use AI to deliver measurable cost savings and margin improvements over those that rely on superficial features. Additionally, 68% of tech leaders plan to streamline their vendor relationships by cutting their vendor count by 20% this year [1]. This signals a growing preference for platforms that address comprehensive, industry-specific needs.

For SaaS providers, the path forward is clear: specialize deeply, integrate AI effectively, and own the workflow that combines AI with a vertical focus. With $3.7 trillion in global dry powder available [1], companies that can showcase niche expertise, stable cash flow, and defensible positions built on proprietary data and domain knowledge are in the best position to secure future investments.

FAQs

What makes a SaaS product “vertical” vs “generic”?

Vertical SaaS products are designed to meet the specialized needs of a single industry, focusing on the specific and critical workflows unique to that sector. On the other hand, generic SaaS solutions are broader in scope, catering to general-purpose use cases across various industries. This makes them less tailored but often easier for users to switch between.

How do AI agents change SaaS pricing and revenue?

AI agents are transforming how SaaS companies approach pricing and revenue strategies. By automating tasks and offering specialized, high-impact solutions, businesses can justify charging premium prices - particularly in focused areas like enterprise workflows. But here's the catch: investor interest is leaning heavily toward AI-first platforms and vertical SaaS solutions built around proprietary data. This shift makes standing out even more important for general-purpose tools. To stay ahead, SaaS companies need to highlight their distinct AI features and capabilities in this fast-changing landscape.

What proof do PE firms want to see that an AI moat is real?

Private equity firms seek tangible proof of an AI-driven competitive edge. This could include assets like proprietary data that others can't easily replicate, exclusive distribution channels that ensure market access, or an AI-powered operating model that supports scalable growth while remaining difficult for competitors to challenge. Highlighting these strengths signals that the business is well-positioned to sustain its market advantage and provide enduring value.

Related Blog Posts

- From Hype to High-Value Exits: AI's Role in Private Equity's Future

- How to Turn PE from a Threat Into Your Biggest Growth Weapon

- 3. From 2015 to 2025, PE Acquired 1,900 Software Companies for $440 Billion. AI Is Now Dismantling the Thesis Behind Every Single One. Nobody on Wall Street Wants to Say It First. SaaStr

- 12. PE Has $2 Trillion in Dry Powder and a "Deploy or Return" Mandate. Every Dollar Chasing the Same Thesis: Own the Data. Own the Distribution. Everything Else Is Leverage. FinancialContent