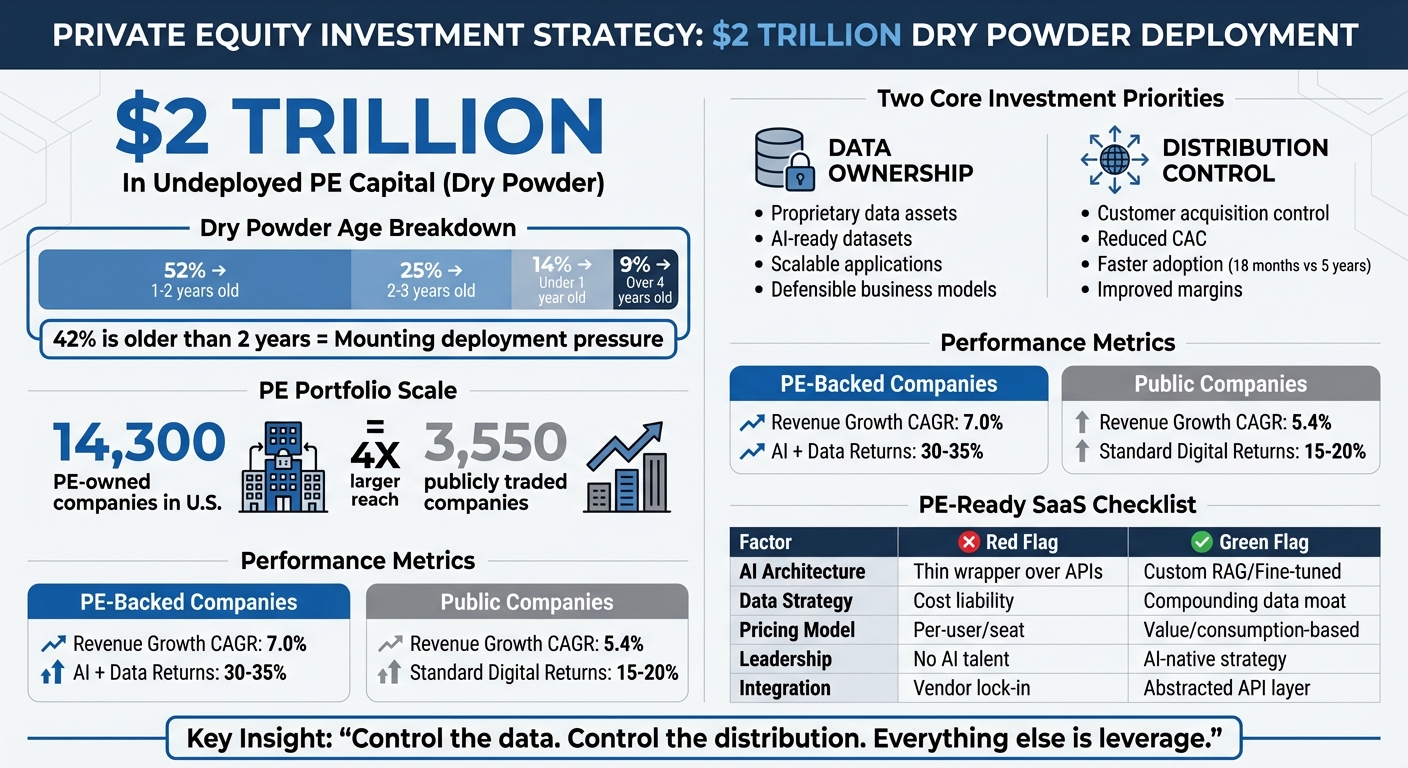

Private equity (PE) firms have $2 trillion in unused capital, known as "dry powder", with a clear mandate: invest it or return it to investors. Rising interest rates and valuation mismatches have slowed deal activity, leaving funds raised in 2021–2022 under pressure to deploy capital before their deadlines. This has driven PE firms to focus on two key investment priorities:

- Data Ownership: Companies with proprietary data assets, especially in SaaS and AI, are highly attractive. Owning unique data enables scalable AI applications and defensible business models.

- Distribution Control: Businesses that control their customer acquisition channels reduce costs, accelerate adoption, and improve margins, making them prime targets for investment.

PE firms are moving away from debt-driven returns and prioritizing assets with built-in structural advantages. The focus is on businesses that can scale quickly, offer predictable growth, and maintain defensibility. Companies lacking these traits risk being overlooked in today’s competitive market.

Private Equity's $2 Trillion Dry Powder: Investment Priorities and PE-Ready SaaS Metrics

Understanding the $2 Trillion Dry Powder Problem

How PE Firms Accumulated $2 Trillion in Undeployed Capital

Private equity (PE) firms are sitting on an estimated $2 trillion in undeployed capital - or "dry powder" - as of early 2026. This buildup stems from a mismatch between aggressive fundraising and more cautious dealmaking. Several factors contributed to this, including the rise of mega-funds requiring numerous transactions, a slowdown in deal activity post-2021, and widening valuation gaps between buyers and sellers due to higher interest rates [1].

Breaking it down, as of 2025, 52% of global buyout dry powder is one to two years old, 25% is two to three years old, and 9% has been sitting for over four years [2]. This means that 42% of the capital is now older than two years, creating mounting pressure on general partners (GPs) to deploy funds within the typical 5-6 year window - or risk returning uncalled capital to limited partners (LPs).

"The industry is not yet under systemic deployment pressure, but the clock is ticking louder for 2021 and 2022 vintages." - PE 150 [2]

This growing urgency is forcing PE firms to intensify their search for assets that offer strong, defensible advantages. The accumulation of aging capital is reshaping how firms approach investments, with a focus on safer, strategically positioned opportunities.

What This Means for SaaS and AI Companies

With deployment deadlines looming, PE firms are shifting their strategy. The old playbook of buying companies, leveraging them with debt, and flipping them for profit is becoming less effective in today’s high-interest-rate environment. Instead, firms are prioritizing businesses with built-in structural advantages - assets that don’t rely on financial engineering to deliver returns. This shift is especially relevant for SaaS and AI companies.

Firms are increasingly drawn to SaaS and AI businesses that control proprietary data sets or own customer acquisition channels. These types of assets provide a level of defensibility that competitors can’t easily replicate. For example, in March 2026, Anthropic began discussions with Blackstone and other PE firms to form a joint venture. The goal? To integrate its Claude AI into portfolio companies, replacing existing enterprise software tools [4]. Similarly, in January 2026, a consortium including Silver Lake and the Saudi Public Investment Fund completed a $56.5 billion acquisition of Electronic Arts [8]. These deals highlight the growing appeal of companies with unique data and distribution advantages, aligning with the PE sector's "deploy or return" mandate.

This strategic shift is also reshaping deal dynamics. PE interest is now concentrated on two ends of the spectrum: platforms valued under $100 million for roll-up strategies, and those above $500 million for institutional stability. The traditional middle market is being squeezed out [2]. For SaaS and AI companies that fall into these favored categories - particularly those with strong data assets or direct customer channels - the next 12 to 18 months could present a rare chance to secure much-needed capital, as PE firms race against the clock to deploy their funds.

sbb-itb-9cd970b

Why Private Equity Prioritizes Data Ownership

Private equity firms see proprietary data as a game-changer. It adds value without requiring additional staff and creates a "data gravity" effect, pulling in applications and workflows seamlessly [14].

How Data Assets Drive SaaS and AI Valuations

In today’s landscape, companies either thrive or risk becoming obsolete based on their data capabilities. Those that serve as the trusted source of data are maintaining or even increasing their valuations, while tools focused on narrow tasks are under pressure. A September 2025 survey found that 47.8% of private equity firms are testing AI tools, but fewer than 11% have scaled effectively. The main hurdle? Fragmented data systems [9].

"AI will not create advantage on its own. Proprietary, well-engineered context will. Firms that develop a true data engine now create the institutional memory and architecture that tomorrow's AI will require."

- Phil Westcott, Founder and CEO, Deal Engine [9]

The challenges faced by traditional data providers illustrate this shift. FactSet's enterprise-value-to-EBITDA ratio dropped from 21 in August 2025 to just 12 by March 2026, slashing its market value from $17.5 billion to $8.4 billion [13]. Morningstar and Gartner faced similar declines, with their ratios falling to 12.6 and 14.8, down from around 20 and 23, respectively [13]. However, despite these drops, their data assets remain highly valuable, making them attractive acquisition targets.

| Company | EV/EBITDA (Aug 2025) | EV/EBITDA (Mar 2026) | Market Value (Mar 2026) |

|---|---|---|---|

| FactSet | 21 | 12 | $8.4 Billion |

| Morningstar | ~20 | 12.6 | N/A |

| Gartner | ~23 | 14.8 | N/A |

These valuation trends have led to a surge in private equity interest, with firms focusing on acquiring strong data platforms.

Recent PE Acquisitions Focused on Data Assets

Recent acquisitions highlight the growing importance of data assets. In March 2026, Hg Capital announced a $6.4 billion deal to take OneStream private. This wasn’t just about software; it was about gaining access to a unified data platform designed for complex financial processes and proprietary financial consolidation rules [12]. Around the same time, Thoma Bravo and Hellman & Friedman explored buying FactSet after its share price dropped 39%, seeing an opportunity in its predictable subscription revenues and deeply embedded data assets [13].

AI-focused companies are also making data-driven moves. In April 2026, OpenAI acquired Hiro Finance, a personal finance startup, to secure proprietary financial data that would enhance its AI tools [11]. Similarly, FactSet partnered with Anthropic in February 2026 to develop new tech tools, resulting in a 6% spike in its stock price in just one day. This demonstrates how established data companies can use AI to strengthen their market position [10].

"As the software market bifurcates, some models will be existentially threatened but, more so, there will be great opportunities. The businesses in truly defensible positions that demonstrate revenue stability will leverage AI as an accelerant."

The takeaway is clear: private equity firms are willing to pay top dollar for companies where data is the product, not just a side feature. If your SaaS or AI company lacks unique data essential for AI functionality, you’re stuck competing on price. But if you own and maintain proprietary data assets, your business becomes nearly impossible to replace.

Why Distribution Control Attracts PE Investment

Private equity (PE) firms have a clear goal: to own the channels through which products are sold. Why? Because controlling distribution slashes customer acquisition costs, speeds up deployment, and boosts profit margins.

The Economics of Owning Your Distribution

Traditional enterprise sales can be painfully expensive and slow. In many cases, it might take up to five years for a new technology to gain traction in enterprise settings. But when a PE firm controls the distribution channel, that timeline shrinks dramatically - often to just 18 months [4].

Here's a staggering number: PE firms now own 14,300 companies in the U.S. That’s nearly four times the number of publicly traded companies, which stands at 3,550 [7]. This vast network gives PE firms a unique advantage. When they prove the value of a tool in one or two companies, they can roll it out across their entire portfolio almost instantly, bypassing the lengthy sales cycles that traditional methods require.

"A private equity firm owning 25 companies proves value in one or two before rolling out to the entire portfolio. Control enables rapid deployment."

- Tom Tunguz, GP at Theory Ventures [7]

The financial results speak for themselves. PE-backed companies achieve 7.0% revenue growth CAGR, compared to 5.4% for public companies [7]. This growth stems from their ability to quickly implement new tools while avoiding high customer acquisition costs through internal cross-selling. It’s a strategy that aligns perfectly with the PE goal of acquiring assets that are both strategic and defensible.

There’s also a sense of urgency driving this approach. With 52% of the $2 trillion in dry powder sitting between one and two years old [2], PE firms are under pressure to deploy capital into scalable assets. Companies that control their own distribution channels offer predictable, low-cost growth without the need for expensive sales teams or reliance on third-party platforms. This control becomes a key driver for sustained and accelerated growth.

PE-Backed Companies That Won Through Distribution Control

The benefits of distribution control are evident in how PE firms execute strategic rollouts. Take March 2026, for example, when Anthropic entered talks with Blackstone to form a joint venture. The goal? Embedding Anthropic’s Claude AI across Blackstone’s extensive portfolio [4]. This wasn’t just a software deal - it was a calculated move to leverage Blackstone's distribution power. By replacing costly horizontal SaaS licenses with custom AI tools, Blackstone cut software expenses across its portfolio and improved margins.

PE-backed rollouts often bypass the drawn-out negotiations typical of enterprise sales. Instead, board mandates enable swift implementation, creating significant value for both the PE firm and the software provider.

"Private equity is essentially pushing AI as a service that eliminates the need for certain categories of software entirely. A replacement cycle that might have taken five years through normal enterprise adoption could compress to 18 months inside a PE portfolio."

- CNBC Commentary [4]

PE firms are no longer just buyers - they're transforming into catalysts for rapid AI-driven software adoption. For example, when Atlassian cut 1,600 jobs (10% of its workforce) to redirect resources toward AI, and Block announced 4,000 AI-related job cuts, their shares surged by 17% [4]. Wall Street clearly saw the potential for expanded margins.

For SaaS and AI companies, the takeaway is straightforward: if you want PE investment, create products that can be deployed quickly across a portfolio without relying on traditional sales teams. Controlling distribution isn’t just an added bonus - it’s the difference between being an expense and becoming a multi-billion-dollar strategic asset.

Case Study: How AgileGrowthLabs Combines Data and Distribution

AgileGrowthLabs stands out as a perfect example of a platform tailored for private equity (PE) firms. Why? It seamlessly integrates data ownership with its distribution channels. This approach checks all the key boxes for PE investments: proprietary assets, low customer acquisition costs, and scalable growth without relying on external platforms. It’s a textbook case of using data and distribution to dominate the market.

AgileGrowthLabs' Approach to Data Ownership

AgileGrowthLabs uses AI-powered data aggregation within its SaaS directory to gain a major edge. By deploying AI agents, the company builds proprietary datasets that competitors simply can’t duplicate. This creates what’s often called a "data moat" - a protective barrier of unique, high-value data. But AgileGrowthLabs doesn’t stop at just compiling tools; it turns that data into actionable revenue intelligence. And as their dataset grows, so does its value. Every click, search, and user interaction enriches this resource, making it a long-term asset that’s irresistible to private equity investors.

But data is only part of the story. The company’s ability to control how it acquires customers is just as important. Let’s dive into that next.

How AgileGrowthLabs Controls Customer Acquisition

On the distribution front, AgileGrowthLabs takes full ownership of its customer acquisition process. By managing direct lead generation, integrating with CRM systems, and automating customer engagement, the company avoids the pitfalls of relying on third-party platforms or costly sales teams. This self-reliant strategy eliminates platform dependency, ensuring steady and scalable growth.

"When strategic fit is clear and the product or talent is globally competitive, valuation becomes secondary - and geography irrelevant" [5].

How to Make Your SaaS or AI Company PE-Ready

If you're aiming to make your SaaS or AI company stand out to private equity (PE) firms, it's all about demonstrating proof - not just potential. With $2 trillion in PE capital waiting to be invested, firms are laser-focused on businesses that have mastered two things: data ownership and distribution control. The key? Building systems that create lasting value through proprietary data and efficient distribution.

Steps to Build Proprietary Data Assets

Start by implementing a "never enter data twice" system. This ensures that once an event is captured, it automatically updates across your platform. It’s a game-changer for accuracy, reducing manual work while keeping your data fresh and reliable in real time [3].

In the first 100 days, prioritize cleaning and organizing your data. Clean datasets are essential for deploying AI effectively and unlocking future revenue opportunities [15]. Instead of pouring resources into expensive foundational models, consider leveraging retrieval-augmented generation (RAG) or fine-tuning with your proprietary data. This approach allows you to differentiate meaningfully without draining your budget [15].

Steer clear of creating products that are just a user interface over public APIs. PE firms see these as risky and lacking long-term defensibility [15]. Instead, focus on building a platform that grows smarter with every customer interaction - a system that compounds value over time [15].

"To command a premium valuation, a target must represent a 'Team + Data Engine' - a proven, production-grade capability already generating value from a proprietary dataset" [15].

Once you’ve built a strong data foundation, the next step is to strengthen your control over distribution channels.

How to Strengthen Your Distribution Control

When targeting customers, aim for PE operating partners rather than individual enterprise leads. Why? As of 2024, there are 14,300 PE-owned companies in the U.S., compared to just 3,550 public companies [7].

"A private equity firm owning 25 companies proves value in one or two before rolling out to the entire portfolio. Control enables rapid deployment" [7].

This approach offers access to entire portfolios and accelerates sales cycles.

Additionally, move away from per-user pricing. As AI automation reduces the need for human headcount, pricing tied to user numbers becomes less relevant and even risky [15]. Instead, adopt value-based or consumption-based pricing models that align with the outcomes or usage metrics your customers care about. To stay flexible and avoid vendor lock-in, abstract your AI model integration behind an internal API layer. This signals to PE firms that your company is built to adapt to changing technologies [15].

| PE Readiness Factor | Red Flag (Low Valuation) | Green Flag (High Valuation) |

|---|---|---|

| AI Architecture | "Thin Wrapper" over public APIs | Custom RAG/Fine-tuned models |

| Data Strategy | Data as a "cost-to-store" liability | Compounding data moat (Data-to-Product) |

| Pricing Model | Traditional seat-based (per user) | Value-based or consumption-based |

| Leadership | Lack of in-house AI talent | AI-native leadership and strategy |

| Integration | Vendor lock-in to a single LLM | Abstracted internal API layer |

Conclusion

Private equity firms are currently holding onto a staggering $2 trillion in available capital. Their directive is clear: deploy it wisely or return it. When they choose to invest, their focus is laser-sharp - control the data, control the distribution. This approach prioritizes operational excellence, especially in today’s high-interest-rate environment, where traditional financial strategies face growing challenges.

Companies backed by private equity that integrate AI with proprietary data are seeing remarkable results. Their return on invested capital nearly doubles, with total returns hitting 30%–35%, compared to the 15%–20% achieved through standard digital upgrades [16]. This highlights just how crucial it is to own and manage high-quality data. As Vrushali Paunikar, Chief Product Officer at Carta, aptly stated:

"If the underlying data is not right, the AI cannot be effective" [3].

Beyond data, controlling distribution channels enhances these returns even further. With private equity firms managing over 14,300 companies, they are in a unique position to accelerate technology adoption timelines - from five years down to just 18 months. On the flip side, SaaS products that lack proprietary data and controlled distribution risk being replaced by internal AI solutions [4].

For SaaS and AI companies aiming to attract private equity investment, adhering to these principles isn’t just a good idea - it’s a necessity for securing top-tier valuations. This means modernizing core systems to ensure data is AI-ready, building proprietary datasets that grow in value with each customer interaction, and targeting private equity operating partners who oversee entire portfolios rather than focusing on one-off enterprise deals.

Looking ahead to 2026, private equity firms will face even greater pressure to deploy their capital [6][17]. Companies that have invested in strong data foundations and secured distribution control will stand out, commanding premium valuations. Those that fail to adapt will find it increasingly difficult to compete. This dual emphasis on data ownership and distribution control defines the private equity investment strategy of today and the near future.

FAQs

What counts as “proprietary data” in a SaaS or AI business?

Proprietary data in a SaaS or AI business refers to exclusive, business-specific information. This can include datasets, CRM systems, market insights, and internal analytics. When combined into a single, intelligent system, this data drives smarter decision-making and helps businesses stay ahead of the competition.

How can a company prove it controls distribution without a huge sales team?

A company can manage its distribution effectively by utilizing data ownership and integrated technology systems. These resources offer access to accurate, real-time data, allowing for streamlined customer relationship management and operational efficiency - all without the need for a massive sales team.

How do PE firms decide between a roll-up platform and a $500M+ “institutional” deal?

Private equity firms often face a choice between pursuing a roll-up platform or engaging in a $500M+ institutional deal, depending on their strategic objectives. Roll-ups involve merging smaller companies to create a larger, unified entity, while institutional deals focus on investing in sizable, standalone assets or businesses. The decision typically hinges on factors such as the desire to achieve operational scale or capitalize on opportunities within particular industries.