The software market is in turmoil. Here's what you need to know:

- $285 billion vanished in one trading day (Feb 3, 2026): Triggered by Anthropic's launch of Claude Cowork, an AI product automating workflows and challenging traditional software models.

- iShares Software ETF (IGV): Down 23% year-to-date, reflecting a $1 trillion loss in enterprise software value.

- Salesforce and Workday: Both saw stock declines of over 40% in 12 months, driven by "seat compression", where AI reduces the need for software licenses.

- AI Spending Boom: Hyperscalers are expected to spend $660–$690 billion on AI infrastructure in 2026, slashing budgets for traditional software.

- SaaS Business Models Under Fire: The per-user pricing model is becoming obsolete, forcing companies to explore usage-based or outcome-based pricing.

Key takeaway: The rise of AI is reshaping the software industry - traditional players must evolve or risk irrelevance.

1. iShares Software ETF

Stock Performance Decline

The iShares Expanded Tech-Software Sector ETF (IGV) experienced a steep fall, dropping from $117 to $82 by mid-February 2026 - a 23.4% year-to-date decline that pushed it into bear market territory [2]. By this point, the total value lost across enterprise software was estimated at a staggering $1 trillion [2].

Adding to the grim picture, the fund's Relative Strength Index (RSI) hit 18, marking its lowest level since 1990 [6]. Price-to-sales ratios also plummeted from 9x to 6x, levels reminiscent of the mid-2010s [2]. Core holdings such as Salesforce, Workday, Adobe, and ServiceNow suffered double-digit losses, further dragging the ETF down. These figures highlight the scale of the downturn and set the stage for examining the forces behind this shift.

Key Contributing Factors

The downturn wasn’t triggered by typical financial problems but by a major shift in how software companies generate revenue. Central to this was seat compression, a new risk where AI agents significantly reduce the number of human users who need software licenses. If AI can handle tasks that once required entire teams, businesses may cut software licenses by as much as 90% [2].

Compounding this, enterprise IT budgets were being reallocated. Hyperscalers were expected to spend $660–$690 billion on AI infrastructure in 2026 - almost double the spending levels of 2025. This surge came directly at the expense of application software budgets [2]. The numbers tell the story: only 71% of S&P 500 software companies exceeded revenue estimates in early 2026, compared to 85% for the broader tech sector [2]. The message was clear: AI is consuming the software budget.

Market Impact

This market upheaval - dubbed the "SaaSpocalypse" - highlighted the existential threat to traditional SaaS models. Hedge funds amplified the pressure, holding $24 billion in short positions against software stocks during the selloff [7]. Jeffrey Favuzza, an equity trader at Jefferies, summed up the bearish sentiment:

"The view is that software will be the next print media or department stores, in terms of their prospects" [2].

The selloff created a puzzling contradiction. Vivek Arya, senior analyst at Bank of America, observed:

"The market is simultaneously pricing AI capex failure and AI destroying all software. Both cannot be true" [2][6].

Yet, despite this paradox, investors punished both hyperscalers for overspending on AI infrastructure and software companies for their perceived vulnerability to AI disruption. By mid-2026, the median SaaS revenue multiple had fallen to 4.0x - the lowest since 2016 [5].

Strategic Implications

The IGV’s decline reflects a broader shift in how software companies are valued. Investors are now differentiating between "systems of record" (like ERP and core finance platforms, which have high switching costs) and "systems of engagement" (workflow tools that could easily be replaced by natural language AI) [6]. This shift was underscored by a surprising valuation inversion: the Russell 1000 Software subsector traded at 32.4x forward earnings, while cyclical semiconductor makers traded at 43.6x [6].

For SaaS companies, survival depends on adapting quickly. The traditional per-seat subscription model is being replaced by usage-based or outcome-based pricing. Meanwhile, enterprises are consolidating their software tools, with the average number of SaaS applications per company dropping 18% in 2025 [5]. Dan Ives, analyst at Wedbush Securities, offered a more optimistic take:

"Software will be the heart and lungs of the AI revolution" [2].

This dramatic decline signals a fundamental market repricing, affecting not just the ETF but the broader enterprise software landscape as well.

sbb-itb-9cd970b

Are we in a 'SaaSapocalypse'? Tech VC explains AI's disruption of software

2. Salesforce

Salesforce's journey reflects the shifting dynamics of the SaaS market as AI continues to reshape the landscape.

Stock Performance Decline

Over the past year, Salesforce's stock dropped more than 40% [2][11]. A notable 11% decline occurred in just five days (February 3–7, 2026), following Anthropic's release of Claude Cowork [2]. By mid-February, the company's year-to-date decline had hit 26% [2]. The situation worsened in May 2024, when Salesforce suffered its largest single-day loss since 2004 - a 20% drop after disappointing Q1 earnings [8].

Despite reporting $41.5 billion in revenue for FY2026, with a growth rate of 10% [11], the market reevaluated Salesforce's worth. This disconnect between its financial performance and market valuation hinted at a broader issue: investors were reassessing the viability of its business model.

Key Contributing Factors

At the heart of Salesforce's challenges is the impact of AI on its traditional per-seat licensing model. Jason Lemkin, founder of SaaStr, summed it up with a stark observation:

"If 10 AI agents can do the work of 100 sales reps, you don't need 100 Salesforce seats anymore - you need 10" [2].

This shift could lead to a 90% reduction in revenue for certain functions as AI replaces tasks previously handled by large teams [2]. Adding to the pressure, enterprise IT budgets are increasingly being diverted from application software to AI infrastructure, which is projected to command $660–$690 billion in 2026 [2]. Furthermore, about 70% of software providers, including Salesforce, report that the costs of GPU compute required for AI features are squeezing profitability [2].

These challenges have significantly shaped investor sentiment, creating a ripple effect across the market.

Market Impact

Salesforce has become a symbol of the broader SaaS market downturn, often referred to as the "SaaSpocalypse." Jeffrey Favuzza, an equity trader at Jefferies, painted a grim picture:

"The draconian view is that software will be the next print media or department stores, in terms of their prospects" [2].

The company's valuation has dropped alongside the sector, with software price-to-sales ratios decreasing from 9x to 6x during the 2026 selloff [2]. However, some analysts see potential amid the turmoil. Billy Duberstein, a technology analyst at The Motley Fool, remarked:

"Salesforce is the cheapest it has ever been, but it is yet to be determined as to whether it will win or lose in the agentic AI era" [9].

In an effort to stabilize the stock, CEO Marc Benioff initiated a massive $25 billion accelerated share repurchase program in March 2026, taking on debt to counter the bearish market [9]. A brief rally followed on February 24, 2026, when Salesforce's Slack announced a partnership with Anthropic to create AI plug-ins for industries like investment banking and HR. This announcement boosted shares by 4% as investors searched for signs of recovery [10].

Strategic Implications

To navigate these disruptions, Salesforce is shifting its business model. The company is moving away from traditional per-seat subscriptions and adopting usage-based or outcome-based pricing, which better aligns with AI-driven workflows [2][11]. Early signs of success are evident - its Agentforce platform has reached $540 million in Annual Recurring Revenue, marking a 330% increase [11].

Jefferies analysts have highlighted Salesforce's strengths:

"We believe CRM's highly customized workflows and large footprint within the enterprise as a system of record make it difficult to be displaced" [12].

Salesforce's role as a "system of record" gives it a competitive edge. Unlike simpler interface-based tools, its deep integration into enterprise operations creates high switching costs that AI solutions struggle to replicate. This advantage is reflected in its valuation, as platform-based companies like Salesforce trade at a 2x premium (8.2x EV/Revenue) compared to traditional SaaS firms (3.9x EV/Revenue) [11].

Additionally, Salesforce holds a 1% stake in Anthropic, valued at approximately $3.8 billion based on Anthropic's $380 billion valuation in February 2026 [9]. This investment serves as an ironic hedge against the very AI-driven disruption threatening its core business model.

3. Workday

Workday, much like Salesforce, is grappling with challenges brought on by AI advancements, though the hurdles it faces are uniquely its own.

Stock Performance Decline

Over the past year, Workday's stock has seen a steep 40% decline [2], reaching its lowest point in five years by February 2026 [13]. Following a missed revenue forecast on February 25, shares dropped another 10% year-to-date [16]. Its 12-month forward price-to-earnings ratio stood at 11.94, even lower than Salesforce's 13.98 [13]. Meanwhile, the broader SaaS market also struggled, with median revenue growth dropping to 12.2% in Q4 2025 from 17% in Q1 2024 [14].

Key Contributing Factors

Workday faces mounting pressure from "seat compression", where AI-driven automation reduces the need for human employees in HR and finance, cutting into the number of paid software licenses. This risk grew when Anthropic introduced Claude Cowork in February 2026 [2]. Following a disappointing annual subscription revenue forecast, over 26 analysts adjusted their price targets downward [13]. Piper Sandler analysts observed:

"In an environment where there is increased scrutinization of every metric amidst the AI debates, the guide likely does not allay investors' general concerns for app layer names." [13]

Compounding these issues, extended sales cycles - especially in government and healthcare sectors - have slowed deal closures as companies tighten software budgets. Additionally, corporate hiring slowdowns and AI-related layoffs, such as WiseTech Global's decision to cut 2,000 jobs [13], have further reduced demand for seat-based HR tools.

Operational challenges have also emerged. In February 2026, Workday laid off 400 employees (about 2% of its workforce) to reallocate resources toward AI initiatives. On top of this, the company faces a class-action lawsuit alleging its AI recruitment tools discriminate based on race, age, and disability [15].

Strategic Implications

These challenges have pushed Workday to reevaluate its business model. The company is striving to establish itself as a "system of record" that AI startups cannot easily imitate. Aneel Bhusri, Workday’s CEO and Co-founder, returned in February 2026 to lead the company through this period of transition. He remarked:

"No amount of vibe coding is going to produce an HR or an ERP system. That kind of complexity is very hard to replicate." [13]

In March 2026, Workday introduced Sana, a conversational AI platform embedded into its HR and finance software [18]. Sana includes three main components: Sana for Workday (a unified interface), Sana Self-Service Agent (capable of automating over 300 pre-built HR and finance tasks), and Sana Enterprise (which integrates workflows across third-party platforms like Salesforce and Jira) [18]. Bhusri highlighted:

"AI only works in the enterprise when it's connected to trusted, deterministic systems, and that hybrid architecture is exactly what Workday is building." [18]

To adapt, Workday is shifting away from traditional per-seat licensing. Instead, Sana is offered through Flex Credits, bundled into existing subscriptions [18]. Early adopters have seen promising results: Berner, for example, reported 90% adoption of Sana within 40 days, allowing them to replace 400 ChatGPT licenses [18]. Bhusri also pointed out that major AI companies - such as Anthropic, Google, and OpenAI - continue to rely on Workday for their internal operations [17].

4. Anthropic's Claude AI

Anthropic shook up the software world with the introduction of Claude Cowork, a product that challenges the traditional per-seat pricing model. This bold move reflects trends already visible in the struggles of companies like IGV, Salesforce, and Workday.

Product Launch Impact

On January 30, 2026, Anthropic quietly released 11 open-source plugins for Claude Cowork on GitHub - no flashy press conferences or events. Yet, the impact was anything but quiet. Within just four days, the software sector saw a $285 billion market cap loss, and the S&P 500 software and services index dropped by $1 trillion between January 28 and early February 2026 [19][20].

Claude Cowork introduced "stack collapsing", offering a single $100/month subscription that could replace multiple software tools at a fraction of the cost. For example, it could handle tasks previously requiring legal review software (over $500/month), CRM add-ons ($150/month), and data analysis platforms ($200/month) - all in one package.

This disruption hit major players hard. Thomson Reuters faced its worst single-day drop on record, with shares falling 15.83% on February 4, 2026, as Claude's legal plugins posed a serious threat to Westlaw and LexisNexis [4]. Likewise, LegalZoom's stock plummeted 20%, and Intuit saw a 10% decline due to competition from finance plugins that rivaled QuickBooks [19].

Key Contributing Factors

Claude Cowork stood out by automating entire workflows. Instead of merely assisting with tasks, it executed them from start to finish, requiring little to no human intervention. Users could describe their goals in plain English - a process Anthropic calls "vibe working" - and the platform would handle complex workflows across multiple systems [19][1].

Its open-source plugin architecture was another game-changer. Teams could create custom sub-agents for areas like legal, finance, and sales without needing to write code. Additionally, enterprise-grade security features, such as virtual machine environments, audit trails, and HIPAA-compliant configurations, addressed corporate compliance concerns [19].

By early 2026, AI-generated code accounted for over 20% of daily GitHub commits, a sharp rise from just 4% at the beginning of the year [19][1]. This surge in AI-driven development underscored Claude's technical sophistication and its potential to reshape the industry.

Market Impact

Claude Cowork's launch forced the software sector to reevaluate long-standing business models. The traditional per-seat licensing approach, a cornerstone of the SaaS industry, faced an existential challenge. Lian Jye Su, a technology analyst at Omdia, remarked:

"Claude Cowork is a direct threat to incumbents like Salesforce, Workday, or ServiceNow, whose models rely on ongoing human interaction with their platforms." [20]

This disruption sent shockwaves through the market. Hedge funds shorted around $24 billion in software stocks in early 2026, while price-to-sales ratios for software companies dropped from 9x to 6x as growth projections were revised downward [19][3].

However, not everyone saw Claude as the end of traditional SaaS. Nvidia's CEO, Jensen Huang, pushed back against the pessimism:

"There's this notion that the software industry is in decline and will be replaced by AI. It is the most illogical thing in the world." [3]

Strategic Implications

Anthropic positioned Claude as a "system of action" through deep enterprise integrations. In February 2026, Snowflake partnered with Anthropic in a $200 million deal, giving its 12,600+ customers same-day access to Claude Sonnet 4.6. This integration powered Snowflake Intelligence and Cortex Code, further embedding Claude into enterprise workflows [19].

Anthropic's CEO, Dario Amodei, highlighted the broader implications for the labor market:

"AI could displace half of all entry-level white-collar jobs in the next 1–5 years." [4]

This raised a strategic dilemma. While Claude threatened to eliminate many junior roles in areas like sales, legal, and finance, it also created demand for experienced professionals capable of managing and orchestrating AI agents. This shift challenges traditional talent pipelines and reshapes workforce dynamics.

Pros and Cons

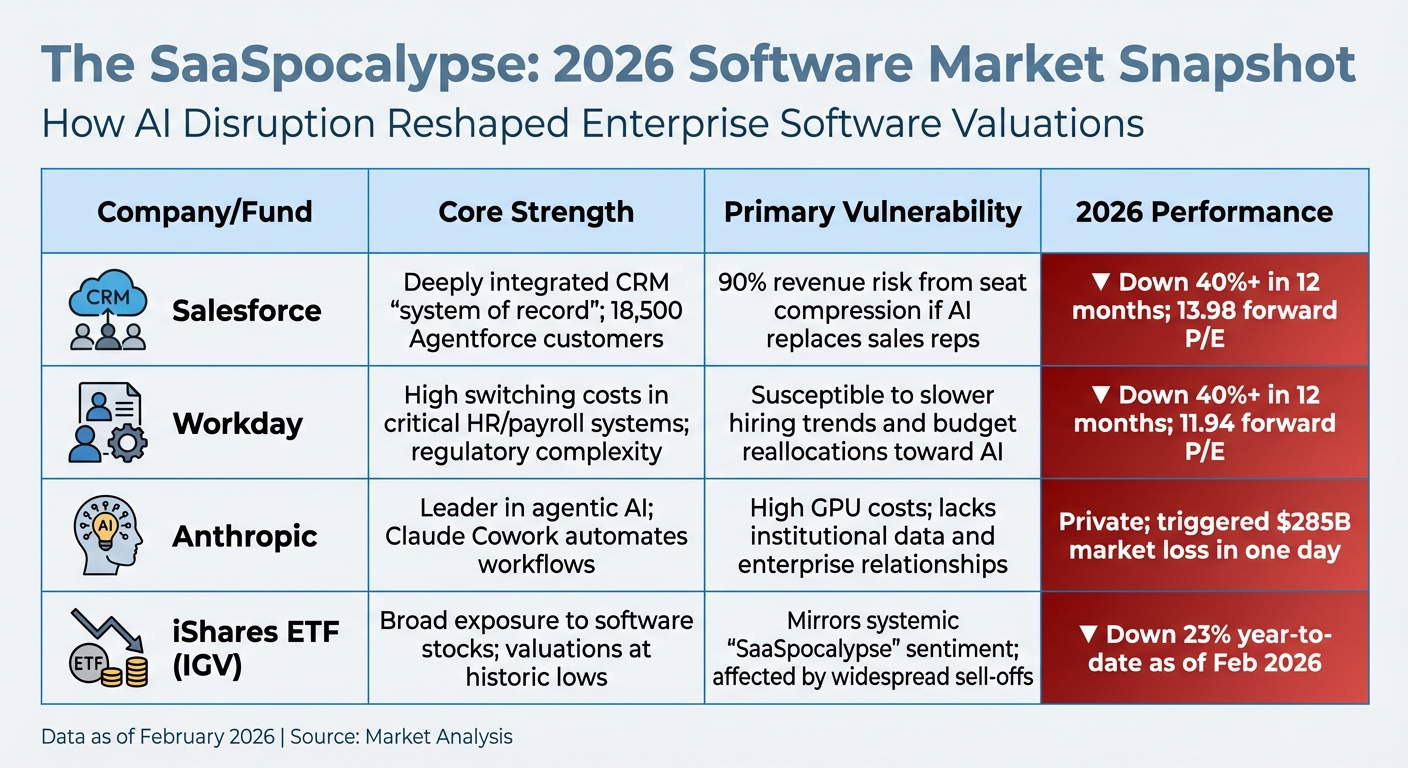

2026 Software Market Crash: Key Players Performance Comparison

This breakdown of pros and cons highlights the broader market dynamics shaping the software sector, especially during the significant downturn seen in early 2026. Understanding the strengths and weaknesses of key players sheds light on the dramatic shifts in the industry.

Salesforce and Workday have long been considered essential systems of record with substantial switching barriers. CEO Aneel Bhusri of Workday has likened replacing their ERP system to "open-heart surgery" [6]. However, the rise of AI-driven tools introduces risks, such as seat compression, which could cut per-seat revenue by up to 90% [2][1]. These vulnerabilities align with the market-wide adjustments brought on by AI disruption, resulting in both companies losing over 40% of their value in the past year [2].

Anthropic, with its autonomous agents, is reshaping workflows and presenting a direct challenge to traditional SaaS platforms [3][1]. However, the company faces profitability hurdles due to high GPU costs and lacks the institutional data and long-standing enterprise relationships that incumbents rely on [2].

The iShares Software ETF (IGV) offers a diversified portfolio of over 100 software stocks but hasn’t been immune to the market's challenges. The ETF has dropped 23% year-to-date as of February 2026, reflecting the widespread sell-off during the so-called "SaaSpocalypse" [2][21]. Analysts at Wedbush Securities argue that enterprises are unlikely to abandon decades of software investments overnight [3].

Here’s a summary of the core strengths, vulnerabilities, and 2026 performance for each player:

| Company/Fund | Core Strength | Primary Vulnerability | 2026 Performance |

|---|---|---|---|

| Salesforce | Deeply integrated CRM "system of record"; 18,500 Agentforce customers [6] | 90% revenue risk from seat compression if AI replaces sales reps [2] | Down 40%+ in 12 months; 13.98 forward P/E [2][17] |

| Workday | High switching costs in critical HR/payroll systems; regulatory complexity [17] | Susceptible to slower hiring trends and budget reallocations toward AI [17] | Down 40%+ in 12 months; 11.94 forward P/E [2][17] |

| Anthropic | Leader in agentic AI; Claude Cowork automates workflows [1] | High GPU costs; lacks institutional data and enterprise relationships [2] | Private; triggered a $285 billion market loss in one day [2] |

| iShares ETF (IGV) | Broad exposure to software stocks; valuations at historic lows [2][21] | Mirrors systemic "SaaSpocalypse" sentiment; affected by widespread sell-offs [2] | Down 23% year-to-date as of Feb 2026 [2][21] |

This table provides a clear snapshot of the competitive landscape and the challenges each entity faces in navigating the evolving software market.

Conclusion

The SaaS landscape is undergoing a dramatic transformation. Declines like the 23% drop in the iShares Software ETF and over 40% losses for Salesforce and Workday, combined with Anthropic's AI plugin launch, signal a shift in how these companies are valued. AI agents, capable of handling tasks traditionally assigned to multiple employees, are challenging the long-standing per-seat licensing model [2].

For investors, this change presents both risks and opportunities. Software valuations have compressed significantly, with price-to-sales ratios dropping from 9x to 6x. Adobe, for instance, now trades at 12x forward P/E compared to its five-year average of 30x [2]. As Vivek Arya from Bank of America points out, the market seems torn between two conflicting narratives:

"The market is simultaneously pricing AI capex failure and AI destroying all software. Both cannot be true" [6].

The key lies in identifying which platforms will endure. Systems of record - those with strong data integration and high switching costs - are better positioned to weather this disruption than more vulnerable systems of engagement [6].

For SaaS companies, adapting quickly is critical. Traditional per-seat subscription models need to give way to usage-based or outcome-based pricing, capturing value from AI-driven productivity rather than human headcount [2]. Moreover, superficial chatbot overlays won't cut it. Companies must integrate genuine, end-to-end AI capabilities to remain competitive.

Enterprise buyers are also rethinking their strategies. By reviewing their software portfolios, organizations can eliminate 20–30% redundancy where AI agents can now take over tasks. These insights can then be used to renegotiate contracts for better terms. This shift is already evident, with the average number of SaaS applications per company dropping by 18% in 2025 [5].

As AI spending surges - projected to hit $660–$700 billion by 2026 - software budgets are shrinking. However, platforms that successfully integrate AI are finding new growth opportunities. Salesforce's Agentforce, which gained 18,500 customers in its first year, is a prime example of how incumbents can adapt to this new era. Companies that embrace this agent-native approach are poised to thrive, while those clinging to outdated models risk becoming the "print media or department stores" of the tech world [2].

FAQs

What is “seat compression,” and how does it reduce SaaS revenue?

"Seat compression" happens when businesses require fewer software licenses - or "seats" - to manage the same amount of work. This shift is driven by AI agents automating tasks that once required human effort.

As a result, companies reduce their subscription counts, which directly impacts SaaS revenue. Traditional per-seat pricing models face disruption as AI takes over roles that previously relied on human-operated tools. This trend marks a fundamental change in how organizations interact with and depend on software.

Which software categories are most vulnerable to AI agents right now?

Software categories that stick to the "per-seat" subscription model - think enterprise SaaS platforms for CRM, legal, financial, or productivity tools - are facing serious challenges. Advanced AI agents, like Anthropic's Claude Cowork, are stepping in to handle tasks such as legal reviews and workflow management. By automating these processes, these tools cut down the need for multiple software subscriptions. This change poses a direct threat to the core revenue streams of traditional SaaS providers, potentially shaking up their valuations in a big way.

How should enterprises renegotiate SaaS contracts in an AI-driven budget shift?

To keep up with AI-driven shifts in SaaS, companies should prioritize outcome-based pricing and flexible contracts. Start by reviewing your current usage to spot unused features or services. From there, negotiate pricing models tied to clear, measurable results rather than traditional metrics. Make sure contracts include options for scaling up or transitioning to AI-powered alternatives as needed.

It's also essential to work closely with vendors. Open communication can help ensure their offerings align with your changing needs. This approach helps move away from outdated per-seat pricing models, allowing you to get the most value in a quickly evolving market.

Related Blog Posts

- From Hype to High-Value Exits: AI's Role in Private Equity's Future

- Why AI SaaS Valuations Are 25.8x Revenue (And Why Your SaaS Might Be Worth More Than You Think)

- 3. From 2015 to 2025, PE Acquired 1,900 Software Companies for $440 Billion. AI Is Now Dismantling the Thesis Behind Every Single One. Nobody on Wall Street Wants to Say It First. SaaStr

- 7. The Private Credit Market Has $600 Billion Bet on Software Companies That AI Is Now Replacing. This Is the Quiet Crisis Nobody Is Tracking.