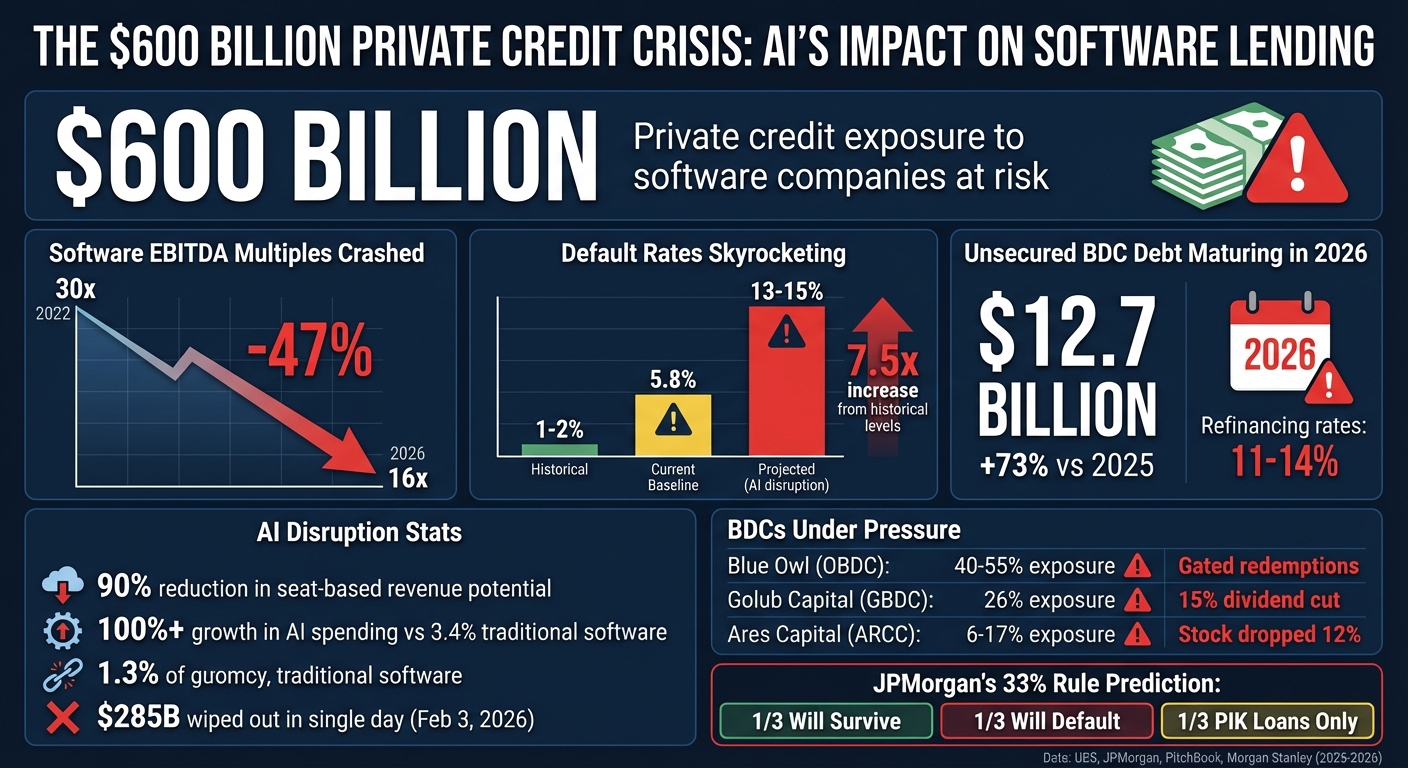

The private credit market is facing a hidden challenge: $600 billion in loans tied to software companies are at risk as AI disrupts traditional SaaS business models. AI tools are replacing expensive software subscriptions, cutting revenue streams and pushing default rates to alarming levels. Software EBITDA multiples have dropped from 30x in 2022 to 16x in 2026, and default rates in software-heavy portfolios could hit 15%, far above the historical 1-2%. Business Development Companies (BDCs) with software exposure are underperforming, with rising non-accrual loans, dividend cuts, and restricted withdrawals.

Key points:

- AI’s automation capabilities are reducing demand for traditional software licenses.

- SaaS companies relying on per-seat pricing or single-function tools are most vulnerable.

- Investors and SaaS founders must act quickly to address financial risks and integrate AI into their strategies.

- $12.7 billion in unsecured BDC debt maturing in 2026 adds pressure to an already strained market.

The convergence of AI disruption and mounting debt obligations is reshaping the software lending landscape. Both investors and SaaS companies need to prioritize cash flow, rethink loan structures, and embrace AI-driven solutions to survive this transformation.

Private Credit Crisis: $600B Software Loan Market Under AI Disruption Threat

How AI is breaking the SaaS business model...

sbb-itb-9cd970b

How AI Is Replacing Traditional Software Solutions

AI is shaking up the software world by automating tasks that used to rely on costly SaaS subscriptions. Businesses are now questioning the need for dozens - or even hundreds - of legacy software licenses when just a few AI agents can deliver the same results. A survey from January 2026 highlights this shift: while budgets for traditional software grew by a modest 3.4%, spending on AI soared by over 100% [7]. This dramatic shift in funding shows just how disruptive AI has become for the traditional software landscape.

And this isn’t just theory - it’s already impacting companies' bottom lines. Take fintech company Klarna, for example. In late 2024, they replaced their Salesforce CRM with a custom-built AI system to handle customer relationship management [7]. By doing so, they eliminated a major SaaS contract entirely. Across industries, similar moves are becoming more common as AI agents prove they can handle tasks traditionally managed by large teams. This trend could reduce seat-based revenue for traditional software vendors by as much as 90% [7].

AI Automation vs. Traditional SaaS Products

The difference between AI and traditional SaaS tools comes down to how they operate. Traditional software depends on human users to log in, navigate interfaces, and manage tasks. AI, on the other hand, works autonomously, requiring little to no human intervention. This leap forward is made possible by "vibe-coding", a technology that allows non-technical users to create complex applications using just natural language. No coding expertise required.

For example, in early 2026, two CNBC reporters with zero coding experience used vibe-coding tools to replicate a fully functional Monday.com dashboard in under an hour [7]. This kind of accessibility is a game-changer, bypassing the need for traditional, button-driven interfaces.

AI is also shaking up pricing models. While legacy SaaS companies charge on a per-seat basis - billing for every user needing access - AI solutions are moving toward outcome-based or usage-based pricing. These models align costs with actual results, making them more appealing to businesses. Startups leveraging AI-generated code from tools like Cursor and Lovable are scaling quickly without dealing with the heavy technical debt or large engineering teams that burden traditional software companies [6]. This shift is putting pressure on legacy SaaS revenue streams and introducing new risks for companies clinging to outdated models.

Software Categories Being Disrupted by AI

Kort Schnabel, CEO of Ares Capital, remarked, "AI would disrupt many software companies with single-function software products that produce content or analyze and visualize data" [2].

Software tools with narrowly defined purposes - like content creation or data analysis - are especially at risk. These tools are being replaced by AI solutions that can handle multiple functions more efficiently.

Derek Hernandez, an analyst with PitchBook, added, "Software companies with these traits face existential margin compression and potential obsolescence as the market bifurcates between AI-native and AI-embedded category leaders and legacy laggards" [2].

This divide between AI-driven innovators and traditional software providers became even more apparent with the launch of Anthropic's Claude Cowork in February 2026. The launch sparked a wave of investor sell-offs in traditional software stocks as the market began to realize that bespoke AI solutions could make many existing software licenses irrelevant [1][6].

The Financial Risks: Why Defaults Are Rising

AI is reshaping loan portfolios, and the fallout is far from a typical economic slowdown. Analysts describe this shift as "structural obsolescence", meaning revenue loss that’s permanent, not just a temporary dip. For instance, if an AI tool replaces a $100,000 annual software license, that income is gone for good [9].

The financial data highlights the severity of the situation. Software EBITDA multiples have plunged - from 30x in late 2022 to just 16x by March 2026. This sharp decline has wiped out equity cushions that lenders rely on to absorb losses [1][9]. The ripple effects are clear: baseline default rates for private credit have risen to 5.8%. UBS Group warns that if AI disruption intensifies, default rates in software-heavy portfolios could skyrocket to 13% to 15%, a dramatic increase from the historical norm of 1% to 2% [1][3].

Adding to the urgency is the "maturity wall." In 2026, about $12.7 billion in unsecured Business Development Company (BDC) debt will mature - a 73% jump from 2025 [1]. These loans will need refinancing at steep rates of 11% to 14%, just as software companies face declining revenues and valuations due to AI competition [9]. Many borrowers can’t generate enough cash flow to manage this debt, forcing them into Payment-in-Kind (PIK) arrangements - where interest is paid by adding more debt instead of cash. Software companies now dominate the PIK loan market, with PIK income making up over 10% of total income for many BDCs [3][9]. This reliance on PIK loans underscores the financial strain across the sector.

Debt Levels and Default Rates in Software Company Loans

Debt levels among software companies have surged over the last decade. By the end of 2025, loan volumes had exceeded $500 billion, accounting for 19% of all direct loans [4]. Many of these loans were issued during the 2021–2022 boom, when high valuations and leverage ratios - between 6x and 8x EBITDA - were considered safe [9].

But those assumptions are falling apart. AI tools are disrupting the "sticky" recurring revenue models that once justified high leverage. Tasks once tied to expensive enterprise software are now handled autonomously by AI, cutting into revenue streams [9][1]. JPMorgan’s "33% Rule" predicts a grim future: one-third of software firms will survive, one-third will default, and one-third will only generate enough cash flow to cover PIK loan obligations [9].

The speed of the decline is staggering. In early 2026 alone, distressed software loans ballooned by $18 billion, reflecting how quickly AI is reshaping the market [8]. Companies that seemed stable just months ago are now breaching loan covenants and scrambling to renegotiate terms [10].

Why BDCs with Software Investments Are Underperforming

The rising default rates are hitting BDCs hard, especially those heavily invested in software companies. The S&P North American Software Index dropped over 20% in early 2026 [9], leading to immediate portfolio losses. At the same time, investors have been pulling funds, creating redemption pressures that some BDCs are struggling to manage.

The impact is stark. BDCs with higher exposure to software firms have underperformed by about 5 percentage points compared to their peers with lower exposure since October 2025 [4]. For example, Blue Owl Capital (OBDC), with software exposure ranging from 40% to 55% in certain funds, saw its stock trade at a 20% discount to Net Asset Value (NAV). In February 2026, it had to "gate" redemptions for a retail-focused fund after a surge in withdrawal requests [1][9]. Similarly, Golub Capital (GBDC), with a 26% software concentration, cut its dividend by 15% in early 2026 due to rising non-accrual loans [1].

Even major players aren’t immune. Ares Management shares fell over 12% in one week in February 2026 after new AI tools from Anthropic threatened the business models of software companies in its portfolio [3]. Ares’ non-accrual rate rose to 1.8%, forcing the company to issue new notes to cover 2026 obligations [3][9].

"Private credit loans to a lot of software companies. If they start going south, there's going to be problems in the portfolio", said Jeffrey Hooke, Senior Lecturer in Finance at Johns Hopkins Carey Business School [3].

A major structural issue lies in the unitranche loan structure, which combines senior and junior debt into one facility. This setup leaves no subordinated debt layer to absorb losses, meaning a 30% drop in a company’s value can immediately erode a BDC’s recovery prospects [9]. With software valuations continuing their decline and AI adoption accelerating, BDCs face tough decisions: either write down loans now and accept immediate losses or extend credit in the hope of a recovery that may never come. The pressure on these lenders highlights how AI is upending long-held investment models in the SaaS sector.

| BDC / Asset Manager | Software Exposure | Recent Impact (Early 2026) |

|---|---|---|

| Blue Owl Capital (OBDC) | 40% – 55% | Stock at 20% discount to NAV; gated redemptions [1][9] |

| Golub Capital (GBDC) | 26% | Dividend cut of 15% [1] |

| Hercules Capital (HTGC) | ~35% | Under scrutiny due to venture debt exposure [9] |

| Blackstone (BXSL) | ~20% | Relative outperformer with 49% LTV ratio [9] |

| Ares Capital (ARCC) | 6% – 17% | Stock dropped 12% in one week; 1.8% non-accruals [3][9] |

Which SaaS Sectors Face the Biggest AI Threat

The level of risk AI poses to SaaS companies depends heavily on their business models. Companies relying on seat-based pricing or offering single-function tools are particularly vulnerable. Why? Enterprises are questioning the need for hundreds of software licenses when a few AI agents can deliver the same results, often more efficiently.

Take CRM and sales tools, for example. Legacy giants like Salesforce, which have long thrived on per-seat subscriptions, are under immense pressure. AI agents can now handle tasks previously managed by entire teams, reducing the need for individual licenses by as much as 90% [7].

Content production and analytics platforms are also feeling the heat. Tools that once specialized in creating content or visualizing data are being absorbed into broader AI-native platforms. What used to require costly subscriptions can now be done in-house at a fraction of the price.

Derek Hernandez, an analyst at PitchBook, summed it up: "Software companies with these traits face existential margin compression and potential obsolescence as the market bifurcates between AI-native and AI-embedded category leaders and legacy laggards" [2].

The financial fallout is already apparent. Software represents about 25% of all private credit lending, with half of the borrowers in this space rated B- or lower, signaling high credit risk [7]. Between October 2025 and February 2026, software stocks plummeted nearly 30% [4], with February 3, 2026, alone seeing $285 billion wiped out in market value [7]. Companies burdened with fragmented data silos and outdated systems are particularly at risk. These firms often lack the infrastructure to train effective AI models or transition from basic "copilots" to fully autonomous "agents" quickly enough to stay competitive [2][11].

Before and After: How AI Changed SaaS Revenue Models

The impact of AI on SaaS revenue models has been dramatic, as shown in the table below:

| SaaS Sector | Traditional Model (Pre-AI) | AI-Disrupted Model (Post-AI) | Revenue Impact |

|---|---|---|---|

| CRM & Sales | Per-seat licensing; revenue scales with team size | Outcome-based or agent-based pricing | 90% reduction in required seats |

| Content Platforms | High-margin subscriptions for specialized tools | AI agents create content at near-zero cost | Commodity pricing; margins collapse |

| Analytics & Data | Specialized tools for manual data visualization | AI agents analyze and act on data directly | Manual dashboards become obsolete |

| Customer Support | Large-scale seat licenses for human agents | Custom AI systems replace third-party tools | Vendors displaced entirely |

These shifts highlight the challenges private credit investors face in an AI-driven market, where traditional revenue models are being upended.

What Investors and SaaS Founders Can Do Now

AI-Based Risk Assessment for Investors

Relying solely on "sticky" Annual Recurring Revenue (ARR) is no longer enough. Investors must shift their focus toward cash flow conversion, market dynamics, and competitive positioning [1]. The critical question isn't just about recurring revenue - it’s whether that revenue can survive when AI agents drastically reduce user counts.

Start by identifying vulnerabilities in your portfolio. Companies burdened with high technical debt, fragmented data systems, or no clear progression from "copilot" tools to fully autonomous "agent" functionality are at significant risk [2].

Derek Hernandez, an analyst at PitchBook, warns, "Credit investors should be most concerned about software concerns with no clear path from copilot to agent, and business models vulnerable to incumbent platform vendors" [2].

Reassess your loan protections immediately. Shift covenants from revenue-based to EBITDA-based metrics within three years to ensure financial discipline as business models evolve [2]. Keep a close eye on Interest Coverage Ratios and Payment-in-Kind (PIK) interest levels - rising PIK can be an early indicator of cash flow issues [1]. UBS Group AG has cautioned that "severe AI disruption scenarios" could push default rates in software-heavy portfolios to 15%, far above the historical 1–2% range [1].

Leverage AI-driven stress testing to model scenarios where "agentic AI" reduces seat counts by 90% while maintaining the same business output [7]. Avoid companies offering narrow solutions that AI agents or bundled platforms can easily replicate [12]. Instead, prioritize businesses with advantages like proprietary data, mission-critical workflows, regulatory barriers, or strong control over distribution channels [12].

While investors must act decisively, SaaS founders also have critical steps to take to adapt to this AI-driven landscape.

How SaaS Founders Can Integrate AI to Stay Competitive

For SaaS founders, speed is everything right now. The market is splitting into leaders who embrace AI and those left behind [2]. The priority? Transition from copilots - tools that assist users - to fully autonomous agents capable of executing complex tasks without human input [2, 17].

Focus on applying AI to streamline physical processes and internal operations that directly improve profit margins [10].

Matt Schwartz, a partner at DLA Piper, emphasizes, "The real risk today isn't having software exposure - it's backing companies that were priced for perfection or that don't have a credible, practical AI strategy" [10].

Adopt outcome-based pricing models instead of per-seat pricing to reflect the efficiency gains driven by AI [12]. While this introduces some revenue variability, it also creates opportunities for significant growth during periods of strong adoption. At the same time, ensure you're passing increased compute and inference costs to customers - absorbing these costs can erode your margins [12].

To stay defensible, build strong moats around proprietary data, deeply integrated workflows, and regulatory barriers [12]. Single-function tools that merely analyze or visualize data are especially vulnerable to being replaced by platform-level AI features [2].

As founders innovate internally, tackling external financial pressures is just as critical.

Refinancing Options for SaaS Companies Under Pressure

With AI reshaping market conditions, strategic refinancing is becoming a necessity for many SaaS companies. If financial pressures are mounting, act now. Early intervention - like negotiating covenant relief with lenders - can prevent breaches and keep you in control. Shift focus from headline ARR to free cash flow, as lenders are increasingly skeptical of "growth at all costs" in today’s environment.

Consider Payment-in-Kind (PIK) interest arrangements to conserve liquidity by rolling interest payments into the principal balance. Renegotiate covenants to replace revenue-based triggers with EBITDA-based metrics, aligning with evolving business models.

In February 2026, Blue Owl Capital’s retail-facing fund (OBDC II) halted redemptions after requests exceeded 15%. To manage liquidity, the fund sold $1.4 billion in loans at 99.7 cents on the dollar to institutional buyers, including CalPERS and two Canadian pension funds [7].

For companies facing deeper financial distress, restructuring capital stacks may be unavoidable.

Brett Pearlman, a partner at Cleary Gottlieb, explains, "Private lenders will have important decisions to make with respect to stressed companies in their portfolios, including whether capital stacks should be recut with the sponsors maintaining control, should lenders 'take the keys,' or should the companies seek to sell off their assets?" [10].

Some businesses are already divesting non-core units to pay down debt and focus on AI-defensible products.

The debt maturity wall is looming. Around $12.7 billion in unsecured BDC debt is set to mature in 2026, a 73% increase over 2025 levels [1]. If your debt is nearing maturity and you lack a solid AI strategy, your refinancing options will be limited. Building a credible AI roadmap now is essential - it may be your only leverage in future negotiations.

Conclusion: Getting Ready for AI-Driven Software Markets

The private credit market tied to software companies is at a critical crossroads. With $600 billion in private credit exposure, the risks are mounting. Software EBITDA multiples have plunged - from 30x in late 2022 to just 16x by March 2026 [1]. Morgan Stanley projects direct lending defaults could spike to 8% [5]. Meanwhile, $12.7 billion in unsecured BDC debt is set to mature in 2026, a staggering 73% jump from 2025 [1]. Clearly, action can no longer be postponed.

The market is now divided into two distinct groups: AI-native leaders who have embraced technologies like autonomous agents and outcome-based pricing, and legacy providers weighed down by technical debt and outdated strategies. With software companies accounting for about 25% of all private credit lending [1], these shifts are impossible to overlook. Investors banking on "sticky" ARR models are staring at potentially steep losses.

Matt Schwartz, a partner at DLA Piper, summed it up: "Software isn't broken - what's changed is that investors are underwriting it like a real business again" [10].

For SaaS founders, the message is clear: adapt or face irrelevance. Companies must integrate AI deeply into their products and pricing strategies to stay competitive. This means breaking down data silos, moving beyond copilots to autonomous agents, and securing intellectual property enhanced by AI. Those that fail to act risk being overwhelmed by mounting legacy debt and an inability to compete in an AI-driven world.

The shift from predictable recurring revenue to an AI-fueled, less certain landscape demands immediate and bold action. With the convergence of AI disruption and the looming 2026 debt maturity wall, hesitation could prove costly for both investors and founders. The time to act is now. Delay is no longer an option.

FAQs

Which software companies are most likely to default because of AI?

Software companies facing the highest risk of default due to AI are those most exposed to AI-driven disruption. This group includes SaaS companies and legacy software providers whose traditional business models and profit margins are under pressure. AI is lowering barriers to entry, making it easier for customers to develop their own solutions, which directly undermines these companies' revenue streams and competitive edges.

How can investors spot AI-driven credit risk before defaults rise?

Investors looking to spot AI-driven credit risks should start by taking a closer look at borrower fundamentals. Are the companies they’re lending to still on solid ground, or are their business models at risk of being upended by AI? This is especially important in industries where AI is making waves, potentially reshaping cash flows and altering long-standing revenue streams.

Another key strategy is to track market sentiment. If the market starts losing confidence in a particular sector or company due to AI disruption, it could signal trouble ahead. Public perception and investor behavior often give early warning signs of vulnerabilities.

Lastly, keep an eye on valuation declines among software companies. Sectors where AI is quickly replacing traditional software solutions are particularly exposed. When advancements in AI start rendering older technologies obsolete, the companies relying on those technologies may struggle to maintain their footing. By focusing on these areas, investors can better anticipate where risks might emerge.

What should a SaaS company do now to refinance safely in 2026?

For SaaS companies aiming to refinance safely in 2026, a proactive approach is essential. Start by reassessing your capital structure to ensure it aligns with both current market realities and your long-term goals. This means evaluating debt levels, interest rates, and repayment schedules to identify areas that need adjustment.

Next, explore refinancing options early. Waiting until market conditions deteriorate could limit your choices or lead to unfavorable terms. By acting ahead of time, you can take advantage of better opportunities and reduce exposure to potential risks.

Finally, focus on maintaining strong cash flow and profitability. These factors not only improve your financial stability but also make your company more attractive to lenders, especially in a private credit market that's constantly evolving due to AI-driven disruptions.

By staying ahead of these challenges, SaaS companies can better navigate uncertainties and secure their financial future.

Related Blog Posts

- From Hype to High-Value Exits: AI's Role in Private Equity's Future

- Is Private Equity Actually Evil? The Truth Might Surprise You.

- Why Buying a Business Beats Starting One in 2025

- 3. From 2015 to 2025, PE Acquired 1,900 Software Companies for $440 Billion. AI Is Now Dismantling the Thesis Behind Every Single One. Nobody on Wall Street Wants to Say It First. SaaStr