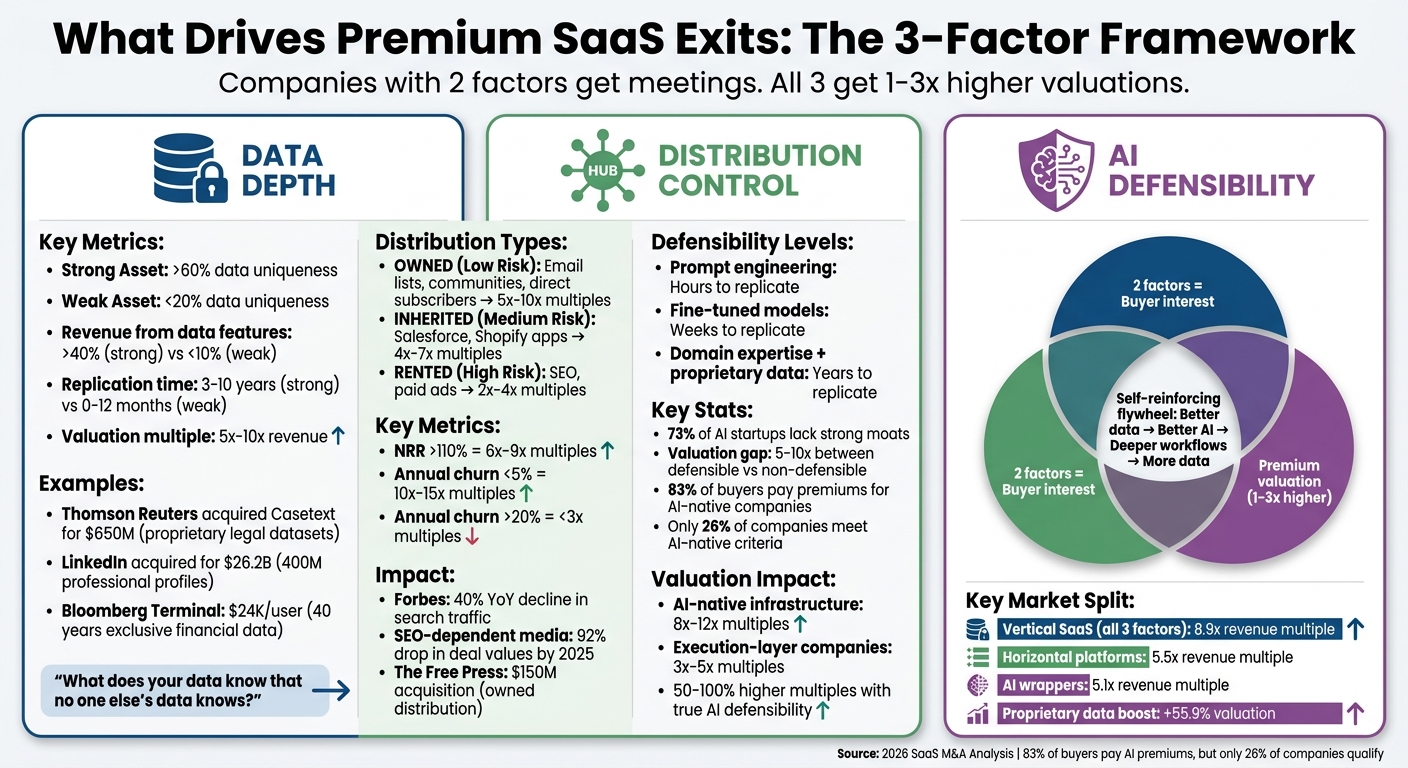

Buyers in 2026 don’t just want high ARR - they’re looking for structural advantages that AI can’t easily disrupt. The three most important factors that determine your exit value are:

- Data Depth: Proprietary datasets that competitors can’t replicate or buy.

- Distribution Control: Channels you own (like direct subscribers or embedded workflows) rather than rented ones (like SEO or paid ads).

- AI Defensibility: Products that can’t be replaced by AI models within 18–24 months.

Companies with two of these factors get buyer interest. All three? You can command premium valuations - often 1–3x higher than competitors. The market is splitting: businesses with strong moats are thriving, while execution-layer companies relying on generic features or SEO are seeing valuations drop.

Key Takeaways:

- Buyers prioritize defensibility over raw ARR.

- Proprietary data, owned distribution, and AI-driven workflows are the new gold standard.

- Without these, expect lower multiples and higher risk of disruption.

The question isn’t just about what your software does - it’s about what makes it irreplaceable in an AI-driven world.

SaaS Exit Value Factors: Data Depth, Distribution Control & AI Defensibility Comparison

Data Depth: Why Proprietary Data Drives Acquisition Value

As buyers increasingly prioritize scarcity and defensibility, proprietary data has become a key factor in boosting a company's exit value. When assessing a business, buyers aren't just looking at what the technology can do - they're diving into the unique insights your data provides. Joash Boyton, Founder & Managing Director of Acquiry, captures this perfectly: "The question is no longer just 'what does your software do?' It is 'what does your data know that no one else's data knows?'" [2].

It’s not about having massive amounts of data - it’s about having data that cannot be replaced. With AI driving down development costs, the real value of your business shifts from execution to the exclusive insights embedded in your data [2].

Proprietary data creates a competitive moat that becomes even more valuable in the AI era. If your product relies on publicly available data that anyone can scrape, advances in AI could quickly erode your edge. On the other hand, products powered by unique, proprietary data gain an advantage as AI unlocks insights competitors simply cannot replicate. This is why companies with strong proprietary data often command valuation multiples of 5× to 10× revenue, compared to 2× to 5× for those without such assets [9].

The difference between basic data and data that drives premiums lies in exclusivity, historical depth, and real-world impact. Take Circana (formerly NielsenIQ) as an example - it dominates retail analytics because of its decades-long collection of exclusive point-of-sale transaction records. Replicating this would require decades of data collection and countless retailer agreements [8]. Similarly, Bloomberg Terminal charges $24,000 per user annually, largely because of its unmatched proprietary financial records and real-time pricing feeds [9].

"The companies that survived the API era owned the graph. The companies that will survive the LLM era own the data."

- Lewis Lin, Author and Strategy Expert [8]

In June 2023, Thomson Reuters acquired Casetext for $650 million. The premium price wasn’t about revenue; it was the proprietary legal datasets and domain expertise that generic AI tools couldn’t match [3]. Similarly, Microsoft’s 2016 acquisition of LinkedIn for $26.2 billion hinged on its irreplaceable dataset of 400 million professional profiles and connection graphs [9]. A telling statistic: 83% of active buyers in 2026 reported paying premiums for AI-native or AI-integrated targets, underscoring the immense value of proprietary data [6].

How to Measure Your Data's Value

When buyers assess data, they focus on four main dimensions: uniqueness, growth in volume, commercial relevance, and the time it would take for competitors to replicate it. If your data can be easily purchased, scraped, or generated synthetically, its strategic value is inherently limited [9].

Start by evaluating how much of your data is genuinely proprietary. Strong data assets typically have over 60% uniqueness - meaning more than 60% of the dataset isn’t available elsewhere. Weaker assets often fall below 20% uniqueness [9]. Next, analyze how much of your revenue stems directly from data-driven features. Businesses with strong data moats often generate over 40% of total revenue from such features, compared to less than 10% for weaker data assets [9].

Growth is another critical factor. A dataset that grows organically by more than 30% annually reflects a reinforcing cycle, while growth below 10% may indicate missed opportunities. Lastly, consider replication time. Strong data assets usually take 3 to 10 years for competitors to rebuild, whereas weaker assets can be duplicated in under a year [11].

For data to significantly impact valuation, it must deliver clear customer value, be rivalrous - meaning your use of it prevents others from gaining similar value - and lack viable substitutes [10]. Long-term data, like 10 years of financial transactions, is especially prized since it can’t be easily synthesized or purchased [2].

| Metric | Weak Data Asset | Strong Data Asset |

|---|---|---|

| Uniqueness | <20% not available elsewhere | >60% not available elsewhere |

| Data-Driven Revenue | <10% of total | >40% of total |

| Replication Time | 0–12 months | 3–10 years |

| Data Volume Growth | <10% annually | >30% annually |

How to Build Proprietary Data Assets

To create valuable data assets, design your product so every customer interaction generates a unique and improving data point. This creates a feedback loop: better data leads to a better product, which attracts more users and, in turn, generates even more exclusive data [9]. Focus on exclusivity and keep your data fresh, whether through proprietary sensors, unique customer interactions, or specialized integrations [11].

Prioritize datasets built over time. For example, 10 years of financial transactions, claims data, or behavioral patterns offer a "longitudinal advantage" that new entrants simply cannot replicate [2]. One notable case involved a global insurance company where an acquirer valued a 22-year proprietary dataset of claims and risk models at $85 million - an asset previously overlooked on the balance sheet [9].

Incorporate data collection into essential workflows. Software integrated into high-stakes processes tends to yield more relevant and harder-to-replace data [2]. Additionally, clear governance - such as documented schemas, data lineage, and strict access controls - can transform raw data into a strategic asset that boosts valuation [9].

Regular audits can help you map and classify datasets by uniqueness, quality, and commercial relevance, uncovering hidden value drivers that might not be reflected on balance sheets. Since accounting standards like IAS 38 often exclude internally developed data assets, it’s crucial to highlight your data moat during due diligence [9].

"Data assets compound in value over time, making them the only asset category that reliably appreciates with use."

- Mark Hillier, CCO, Opagio [9]

Acquisitions Where Data Drove the Price

Several acquisitions highlight how proprietary data translates into premium valuations. For example, in October 2025, The Free Press was acquired for $150 million. Its value wasn’t tied to traffic metrics but to its owned distribution channels and direct subscriber base, showcasing the defensible power of proprietary audience data [2].

Similarly, Brandwatch acquired Basumo at a valuation of 3× to 4× revenue on $450,000 MRR. The key driver? Basumo’s unique content-sharing data and a 400,000-user freemium base that competitors couldn’t replicate. This data asset accelerated Brandwatch’s product roadmap and provided exclusive insights into content performance [12].

"The data is the product... The data moat is not the model architecture - any competitor could build a similar model - but the dataset that powers it."

- Mark Hillier, CCO, Opagio [9]

These examples underscore that companies with robust proprietary data moats often trade at higher revenue multiples - 5× to 10× - while those without such assets trade closer to 2× to 5× [9]. As AI continues to commoditize execution, the key question remains: "What does your data know that no one else's data knows?" [2]

sbb-itb-9cd970b

Distribution Control: How to Build Defensible Customer Channels

Strong distribution control is just as critical as proprietary data and AI defensibility when it comes to commanding a premium exit. While proprietary data acts as a knowledge moat, distribution control ensures you can reach and retain customers without relying on platforms that might change their rules at any moment. Buyers are willing to pay more for companies that own their customer relationships rather than "rent" them from platforms like Google, Facebook, or app stores. The difference is key: owned distribution grows in value over time, while rented distribution demands constant payments for every new customer, offering no lasting advantage [16].

This issue has become more urgent. Publishers that rely on SEO have seen referral traffic plummet by 15% to 40% after Google rolled out its AI Overviews [2]. Forbes experienced a 40% year-over-year decline in search referral traffic, and SEO-dependent media companies saw a staggering 92% drop in deal values by 2025 [2]. When your distribution depends on someone else’s algorithm, a single update can drastically devalue your business.

"AI cannot fabricate real-time liquidity, courier density, reputation history, or a canonical identity graph. Marketplace density and trust are structural, not labor-based."

- Tanay Jaipuria, Partner, Wing VC [2]

Strong distribution control creates what buyers call "workflow gravity" - your product becomes so integral to daily operations that switching would mean overhauling core processes. This isn’t about user familiarity or habits that a better interface could disrupt; it’s about operational switching costs. When leaving your platform requires rebuilding institutional memory, reconfiguring integrations, and retraining teams, you’ve built a moat that even AI solutions can’t easily bypass [21].

The February 2026 "SaaSpocalypse" serves as a stark example. While $285 billion in market capitalization evaporated across software companies, businesses with strong distribution control - like vertical SaaS, trust-based marketplaces, and regulatory-embedded workflows - held steady. Meanwhile, horizontal productivity tools saw their valuations shrink [14][2]. Buyers are clear: if you don’t have a distribution moat, expect a lower valuation multiple [14].

The Types of Distribution Control That Matter Most

Not all distribution channels offer the same level of defensibility. Buyers typically categorize them into three tiers: owned distribution, inherited distribution, and rented distribution.

- Owned distribution: This includes email lists, direct subscribers, private communities, and partner networks. These channels are the gold standard because they grow over time and give you direct access to customers without intermediaries. For instance, The Free Press was acquired for $150 million in October 2025, thanks largely to its owned distribution channels and direct subscriber base - not just its traffic metrics [2].

- Inherited distribution: This involves embedding your product into established ecosystems like Salesforce, Shopify, or Slack. By aligning with trusted platforms, you can inherit their customer trust and intent. To make this strategy stick, your product needs to feel like a natural extension of the platform, not just an add-on [15][16].

- Rented distribution: Channels like paid ads, SEO, and app store rankings fall into this category. These require ongoing costs for every customer acquired and offer little protection when platform rules change. With 80% of consumers relying on zero-click search results in at least 40% of their searches, SEO-dependent businesses are increasingly at risk of losing visibility - even with strong rankings [2].

| Distribution Type | Risk Level | Cost Structure | Defensibility | Buyer Valuation |

|---|---|---|---|---|

| Owned (email lists, communities) | Low | Initial investment, builds over time | High | Premium multiples (5x–10x) |

| Inherited (Salesforce, Shopify apps) | Medium | Platform fees, integration | Medium-High | Stable multiples (4x–7x) |

| Rented (SEO, paid ads) | High | Recurring per customer | Low | Compressed multiples (2x–4x) |

How to Strengthen Your Distribution Moat

To build defensible distribution, you need to integrate it into your product roadmap - not treat it as an afterthought. Start by analyzing how much of your traffic and revenue comes from owned versus rented channels. The goal? Shift toward direct, platform-independent customer relationships [16][2].

One effective approach is deepening workflow integration through the "integration ladder." This framework includes four levels:

- Notifications: Alert users about events.

- Actions: Allow users to respond directly within your interface.

- Automation: Handle multi-step workflows without human input.

- Governance: Become the control layer for compliance, permissions, and audit trails - making your software nearly irreplaceable without a major overhaul of critical processes [16].

Another strategy is community-based distribution. Instead of targeting broad themes like "AI", focus on specific professional groups, such as "recruiters using AI for sourcing" or "finance teams automating reconciliation." This builds relationships and a shared history that technology alone can’t replicate [20][16].

Viral mechanisms are also powerful. Design features that naturally involve collaboration - like shared reports, approval workflows, or review processes - that bring new users into your platform. This way, distribution becomes a built-in feature rather than a separate effort [15][16].

Finally, define your growth strategy with a clear "wedge sentence":

"We grow because [Channel] delivers [ICP] at [Moment of Need] with [Advantage]."

For example: "We grow because Shopify agencies install us during store builds, delivering e-commerce brands at their moment of highest setup urgency with pre-built compliance templates." This focus ensures you prioritize effective channels over spreading resources too thin.

"In the AI application layer, 'better product' is table stakes. Distribution is the separator."

- Curtis Pyke, AI Specialist, Kingy AI [16]

Building strong distribution channels not only secures customer relationships but also significantly impacts your valuation.

How Distribution Control Affects Your Exit Multiple

Strong distribution control directly influences valuations by proving you can retain customers and defend market share - even as AI makes feature replication easier. Buyers often look for Net Revenue Retention (NRR) above 110% as a sign of structural defensibility and strong customer relationships [1][19]. Companies that meet this standard typically command revenue multiples of 6x to 9x, compared to 3x to 5x for those with weaker retention [19].

Top-performing companies with annual churn below 5% and Gross Revenue Retention (GRR) above 95% can achieve multiples of 10x to 15x. On the other hand, businesses with over 20% churn often struggle to reach 3x multiples [19].

In 2025, 72% of all SaaS deals included an AI component, and 80% of buyers reported paying higher valuations for AI-native companies [18][1]. However, this premium only applies when AI strengthens distribution control - such as by improving retention or enhancing customer stickiness. Without measurable results, AI claims can actually create skepticism, which reduces valuations [18][17].

"AI claims without measurable results don't create upside. They create skepticism, and skepticism shows up in valuation."

- Paul Lachance, Senior Managing Director, Software Equity Group [18]

The divide in the M&A market underscores this reality. Vertical SaaS companies with NRR above 110% and strong API dependencies maintain or even increase their multiples. Meanwhile, horizontal productivity tools with high churn and seat-based pricing see their valuations shrink. Trust-based marketplaces and regulatory-embedded workflows continue to command premiums because they own customer relationships that AI can’t easily replicate [2].

AI Defensibility: Making Sure Your Product Can't Be Easily Replicated

AI defensibility plays a critical role in determining whether your product is seen as a premium solution or just another generic option. A staggering 73% of AI startups lack strong protective barriers[11]. This shortfall can result in valuation gaps of 5–10× between companies with enduring competitive advantages and those without[11]. In February 2026, over $1 trillion in market value vanished from software stocks after investors realized that AI agents could replicate much of the functionality offered by generic software[22]. If your AI features can be duplicated by models like ChatGPT or Claude, potential buyers may hold off, expecting a cheaper, commoditized alternative.

The real question isn't just whether your AI works today - it’s whether it becomes more valuable as foundation models improve. If an advanced model like GPT-5 or Claude 4 can replicate your core functionality, your product risks being labeled as just a "wrapper." On the flip side, if these improvements enhance your product by leveraging proprietary data or deep workflow integration, your AI gains lasting defensibility. Companies with such advantages often achieve valuation multiples that are 50–100% higher[25].

"The next generation of great SaaS companies won't be defined by what their AI can build. They'll be defined by what their AI can't replace."

- Steven Cen, Co-founder, ChartGen AI[23]

True AI defensibility requires structural advantages that go beyond surface-level features. This includes owning proprietary data, embedding AI into critical workflows, and operating in regulated environments where compliance creates natural barriers. For instance, Bloomberg sustains its $24,000-per-seat Terminal pricing by leveraging 40 years of exclusive financial data and editorial logic tailored for financial analysts[8]. Similarly, Epic Systems holds a commanding position in healthcare by managing longitudinal health records for one-third of the U.S. population, reinforced by strict regulatory requirements[8].

The M&A market reflects this divide. Companies with integrated, defensible AI solutions attract premium valuations, while tools lacking these protections face declining valuations[25][2]. Additionally, AI has drastically shortened product differentiation timelines for B2B SaaS by 60–80%, enabling competitors to replicate features quickly[24]. Ultimately, relying solely on code as your moat is no longer enough.

How to Test If Your AI Can Be Replaced

Before paying a premium, buyers carefully assess whether your AI features offer lasting defensibility. A useful framework is the "10× Base Model" Test: if the underlying foundation model improves tenfold in a year, does your product become more valuable by leveraging proprietary data and workflows, or does it become redundant? If your product falls into the latter category, it’s just a wrapper.

Another key evaluation is the "30-Second Claude" Test. If someone can describe your core function to a model like Claude or ChatGPT in 30 seconds, and it captures 80% of your value proposition, your AI is vulnerable. Buyers also consider how long it would take to replicate your solution. While prompt engineering can be copied in hours, fine-tuned models offer moderate protection (replicable in weeks), and systems built with domain expertise or human-in-the-loop processes can take years to duplicate[13].

Ask yourself: could a competitor replicate your core functionality within six months? If your system relies on years of proprietary data, specialized expertise, or deep integration into customer workflows, it’s far less likely to be easily replaced.

How to Make Your AI Harder to Replicate

To build defensible AI, you need to create long-term structural advantages that go beyond basic features. Start by developing data flywheels - systems where user interactions continually improve your proprietary AI. This data should be non-synthetic, grow in value over time, and become an essential tool for client decision-making[24][8]. For example, OSIsoft (now part of AVEVA) uses its PI System to collect 20 years of sensor data from production lines, creating a dataset grounded in real-world conditions that general AI models can’t replicate.

Another critical strategy is deep workflow integration. By embedding AI into the operational backbone of businesses - supporting decision automation and institutional memory - you make replacement a complex, strategic challenge rather than a simple technical swap. This type of integration, often referred to as "Layer 4" or "Layer 5" defensibility, requires years of domain expertise and institutional knowledge to replicate[13]. Operating in regulated industries also creates a "regulatory moat", as compliance with frameworks like HIPAA, FedRAMP, or PCI adds barriers that generic AI models can’t easily overcome[22].

Other effective strategies include:

- Model specialization: Fine-tune your AI on exclusive, domain-specific datasets (e.g., training on 500,000 legal contracts with proprietary annotations) to outperform general-purpose models.

- Human-in-the-loop systems: Incorporate expert feedback to continually refine AI outputs, improving reliability and accuracy over time.

- Intangibles: Build brand trust, ensure product quality, and execute rapidly - qualities that take years to develop and can’t be mimicked by AI alone[23].

Companies That Built Defensible AI Products

Several companies demonstrate how strong AI defensibility translates into premium valuations. For example:

- Bloomberg Terminal: Its $24,000-per-seat pricing is sustained by a unique logic layer and decades of proprietary annotations, which support financial analysis in ways general AI cannot match[8].

- Epic Systems: By managing longitudinal health records for one-third of the U.S. population, Epic creates significant switching costs through regulatory compliance and deep workflow integration[8].

- Westlaw: While startups like Harvey offer modern interfaces, Westlaw’s 150 years of annotated case law and editorial insights provide a robust foundation for AI-driven legal research that generic models can’t replicate[8].

These examples highlight the importance of combining proprietary data, workflow integration, and regulatory barriers to create truly defensible AI products. Companies that achieve this balance often enjoy premium valuations and long-term market leadership.

How to Combine All Three Factors for Maximum Exit Value

Integrating the core components - data depth, AI defensibility, and distribution control - lays the foundation for achieving a premium exit. Each element plays a vital role: data depth powers your AI, defensibility makes replication difficult, and distribution control ensures strong customer relationships. Together, they create a "scarcity premium" that sets your company apart in ways AI alone cannot disrupt [2].

The real value lies in the combination. While excelling in two areas can make your company appealing, mastering all three builds a moat that commands significantly higher valuation multiples - 1–3x more than non-AI competitors [1][6]. By 2026, 83% of buyers reported paying premiums for AI-native or AI-integrated companies, but only a small percentage of businesses met the criteria to earn those premiums [6].

The magic is in the synergy. Proprietary data becomes far more valuable when it powers AI models deeply embedded in essential workflows, accessed through direct, algorithm-independent channels [2][5]. This creates a self-reinforcing loop: better data improves AI, which further integrates into workflows, generating even more proprietary data. Buyers pay for this "flywheel effect", not just for isolated features.

How Buyers Score Your Company

Acquirers use a four-tier framework to evaluate companies: No AI, Limited AI Use (e.g., chatbots), AI-Driven (AI as a core strategy), and AI-Native (built entirely around AI) [6]. However, your tier alone doesn’t guarantee a high valuation. Buyers dig deeper into four key areas: the impact of AI on retention metrics, the strength of your proprietary data, the depth of your workflow integration, and how quickly your data flywheel compounds value [1].

Retention is a major signal. Buyers care less about flashy product roadmaps and more about metrics like Net Revenue Retention (NRR) and Gross Revenue Retention (GRR). For instance, a niche SaaS with 115% NRR often looks more attractive than a fast-growing horizontal tool with just 90% NRR because it signals stronger customer lock-in [7]. By 2026, buyers expected 61% of acquisition targets to be AI-driven, but only 26% of companies evaluated in 2025 met that benchmark [6].

Buyers also perform "displacement analysis" to see if a well-funded competitor could replicate your core functionality within 18 months [6]. If your data is publicly sourced, your distribution relies on SEO or paid ads, or your AI is just a thin layer over public APIs, your valuation may suffer. The market has split into two extremes: premium assets with structural advantages attract intense competition, while execution-layer companies trade at lower revenue multiples (3x–5x) compared to AI-native infrastructure businesses (8x–12x) [14][2].

Here’s how buyers categorize SaaS companies based on AI risk and acquisition appeal:

| SaaS Category | AI Threat | Acquirer Appetite | Multiple Direction | Key Signal |

|---|---|---|---|---|

| Deeply Integrated Vertical SaaS | Low | High | Stable / Rising | NRR >110%, API dependency |

| Proprietary-Data SaaS | Low–Medium | High | Rising | Data moat, API access |

| Horizontal Productivity SaaS | Very High | Low | Compressing | Seat-based pricing, high churn |

| Generic Developer Tools | High | Very Low | Compressing Fast | Displacement by AI agents |

Buyers value NRR over raw ARR growth because it reflects structural lock-in and AI-driven workflows [1][7]. To address valuation gaps in AI-heavy deals, they often use contingent structures like earnouts tied to NRR or gross margin targets [4]. AI risk doesn’t always force a sale, but it does demand strategic decisions [6].

Companies That Mastered All Three Factors

Recent acquisitions highlight how integrating these factors drives high valuations.

- CCC Intelligent Solutions acquired EvolutionIQ for $730 million in December 2024. EvolutionIQ combined proprietary data (bodily injury claims), deep workflow integration (insurance carriers), and defensible AI that claims adjusters trusted. Despite raising only $63 million, they secured a significant exit [28].

- Cognigy, a leader in conversational AI, was acquired by Nice for $955 million in 2025, achieving a 15x forward revenue multiple. Cognigy excelled with proprietary data (hundreds of millions of customer interactions) and distribution control (1,000+ global brands like Mercedes-Benz) [26].

- Own (formerly OwnBackup) reached a $2 billion acquisition by Salesforce by focusing solely on the Salesforce ecosystem. This strategy created immense switching costs, as Own became the go-to solution for SaaS data protection within that ecosystem [27].

"AI cannot fabricate real-time liquidity, courier density, reputation history, or a canonical identity graph. Marketplace density and trust are structural, not labor-based."

- Tanay Jaipuria, Partner, Wing VC [2]

- In early 2026, Meta acquired Manus for $2 billion after the AI startup reached $100 million ARR in just eight months. Manus built a sophisticated application layer atop existing models like Claude and OpenAI, focusing on execution and distribution. This demonstrated how the real value now lies in application layers, not just foundational models [29].

These companies didn’t just create AI features - they built structural advantages that made them harder to replicate. As models like GPT-5 and Claude 4 improve, their value only grows because smarter AI amplifies their proprietary data and workflow integrations.

Tools and Resources to Improve Your Exit Readiness

To prepare for a premium exit, audit your business for structural advantages. Distinguish between durable moats - like proprietary data, regulatory licenses, and workflow lock-in - and fleeting ones, such as simple integrations or features AI can replicate quickly [14]. Use the "10× Base Model" test: if foundational AI models improve tenfold, does your product become more valuable or redundant?

Prioritize AI initiatives that improve NRR, GRR, or gross margins, rather than chasing flashy features [1]. Design products to capture "data exhaust" - unique data generated through usage - to fuel self-reinforcing flywheels [5]. Shift to owned distribution channels like email or newsletters to avoid reliance on third-party algorithms that AI is disrupting [2].

Platforms like AgileGrowthLabs and DevelopmentCorporate can guide you through M&A prep, helping document your data moat and verify intellectual property ownership [6][7]. These tools also help navigate the technical scrutiny buyers apply to AI-native companies, ensuring your AI outputs are independently verified to avoid liability [8].

Vertical specialization can also enhance defensibility. Tailor AI models to meet specific industry regulations (e.g., HIPAA or FINRA) and niche use cases where general-purpose models fall short [5]. Focus on perfecting one vertical or problem before expanding, as premature scaling can weaken your business’s core strengths [27][28]. Use AI to measure why customers choose your product and leverage those insights during due diligence to defend your valuation.

Conclusion: How to Prepare Your Business for a Premium Exit

The acquisition market today is a different playing field. If you're aiming for a premium exit in 2026, relying solely on ARR growth won't cut it anymore. Buyers now focus on three critical areas: data depth (exclusive datasets competitors can't replicate), distribution control (channels you own rather than relying on third-party platforms), and AI defensibility (advantages that make your business hard to displace). Nail two of these, and you'll get buyer interest. Master all three, and you could see valuation multiples 1–3x higher than your peers [1][6].

Even with SaaS M&A deal values dropping 77% since 2021, companies with solid structural advantages are maintaining or even increasing their multiples [2]. Interestingly, while 83% of buyers are willing to pay premiums for AI-native businesses, only 26% of companies meet that bar [6]. This mismatch is a golden opportunity for founders who think ahead rather than react to market shifts.

"The question is no longer just 'what does your software do?' It is 'what does your data know that no one else's data knows?'" - Joash Boyton, Founder & MD, Acquiry [2]

Buyers are drawn to businesses with data moats, workflow integration, and owned distribution. On the other hand, companies relying on SEO-driven traffic, seat-based pricing, or features that are easy to copy face valuation pressures. For instance, vertical SaaS solutions are commanding an 8.9x revenue multiple, compared to 5.5x for horizontal platforms and 5.1x for AI wrappers. Proprietary data alone can boost valuations by 55.9% [34].

What Founders Should Do Next

Start by diagnosing your business. Does it fall into "scarcity" categories like proprietary data, owned distribution, or regulatory moats? Or is it in "execution" categories like tools dependent on SEO traffic or generic features? If over 40% of your traffic or revenue comes from Google organic search, it's time to build owned channels like email lists or direct subscribers. AI-driven tools have already cut publisher traffic by 15–40%, making third-party dependencies a risky bet [2].

Next, rethink your data. Is it a strategic asset or just operational output? Buyers care less about what your software does and more about the unique insights your data provides. Longitudinal data - spanning years of real-world activity - has far more value than synthetic or easily purchased datasets. Also, ensure your contracts clearly outline data ownership to avoid legal headaches post-acquisition [2][35].

Evaluate your AI defensibility. Ask yourself: could a well-funded competitor replicate your core offering in six months? If yes, you lack the edge buyers are looking for. Instead of treating AI as an add-on, make it a core part of your product [2][31].

Operationalize AI internally to cut costs and boost margins. Assign engineers to automate workflows in areas like legal, marketing, and finance. These savings can fund proprietary data collection and AI initiatives without needing extra capital [31][32]. Also, consider shifting from seat-based pricing to consumption- or outcome-based models. This approach aligns revenue with the value AI delivers and shields you from pricing erosion as automation reduces labor needs [30][31].

Finally, tighten up your operations. Buyers want to see systems that can run without the founder's involvement. Move sales and support to scalable platforms that can operate independently for at least 90 days before listing. Audit AI-generated code to ensure reliability in critical areas like authentication and error handling. And keep a CRM of your last 20 closed-won accounts - buyers often value a strong acquisition pipeline more than flashy new features [36].

"A shiny feature list gets discounted on sight; a boring, well-documented acquisition pipeline gets paid for." - Tomáš Cina, CEO, Discury [36]

Resources for Building Exit Value

Use a triage framework to allocate resources wisely. Classify your assets into three categories: "Resilient" (invest heavily), "Reinforce" (strengthen moats first), or "Structural Risk" (exit or harvest quickly) [33]. Focus on vertical depth rather than horizontal expansion - vertical SaaS solutions command a 61.8% valuation premium because their domain-specific data and compliance are harder to replicate [34].

Track metrics that matter to buyers. For AI, tie initiatives to improvements in Net Revenue Retention (NRR) or Gross Revenue Retention (GRR). Buyers expect NRR above 110% for vertical SaaS and are wary of companies that can't link AI efforts to measurable retention gains [1][7]. Also, monitor gross margins by customer segment and ensure visibility into usage costs - buyers often stress-test for 25% higher inference costs during due diligence [35].

"AI claims without measurable results don't create upside. They create skepticism, and skepticism shows up in valuation." - Paul Lachance, Software Equity Group [18]

For distribution, prioritize engagement depth over audience size. High email open rates (above 35%) signal strong owned distribution, while large subscriber counts with low engagement suggest dependency on external platforms [2]. Reclaim wasted capital from unused software licenses through SaaS Management Platforms, and reinvest it into AI pilots without diluting ownership [31].

The clock is ticking. With 39.4% of SaaS founders accelerating their exit plans due to AI disruption concerns [6], there's limited time to build the structural advantages that buyers reward. Start taking action now to set your business up for a premium exit.

FAQs

How do buyers verify that my data is truly proprietary?

Buyers assess the exclusivity of your data by looking at its origins. Data sourced from unique relationships, trust, or hard-to-replicate behavioral signals stands out. On the other hand, data that's simply aggregated or based on general access is easier to replicate, making it less appealing. Showing how your data provides a distinct edge can significantly boost its proprietary value.

What counts as “owned distribution” for a SaaS business?

Owned distribution in a SaaS business refers to having direct control over the ways customers are brought in and engaged. This could involve tools like embedded workflows, proprietary data sets, or integrated vertical solutions. Instead of depending on external marketing efforts or third-party platforms, owned distribution allows your business to manage critical customer interactions firsthand.

How can I tell if AI will replace my product in 24 months?

AI has the ability to replicate even the most intricate features at an impressive pace. This means that if your product’s edge lies in aspects that are easy to duplicate, it could face significant challenges. To stand out and remain competitive, focus on durable advantages - those that are harder for others to replicate.

Key strengths to consider include:

- Proprietary data: If your product relies on exclusive data that others can’t access, it becomes much harder to replicate.

- Workflow integration: Products that are deeply woven into users’ daily workflows are harder to replace because switching disrupts established processes.

- Trust and reputation: Building strong relationships and credibility with your users can create a barrier that AI alone can’t overcome.

- Ecosystem connections: Seamless integration with other tools or platforms creates a network effect, making your product more indispensable.

On the flip side, products that depend primarily on execution or features that can be easily copied are more vulnerable. If your product is not anchored by unique data, network effects, or deep workflow integration, it may face the risk of being outpaced by AI-driven competitors.

Related Blog Posts

- "How our AI exit optimization system helped 12 SaaS companies exit for 3-5X industry average"

- SaaS Exit Multiples 2025 How Founders Are Securing 7x ARR Deals

- 1. PE Isn't Buying Your SaaS Company. They're Buying Your Customer Data and Your Distribution List. The Rest Is Filler.

- 16. The Era of "Growth at All Costs" Is Over. The Era of "Whoever Controls the Data Controls the Exit Multiple" Has Begun. Most Founders Are Still Playing the Old Game.