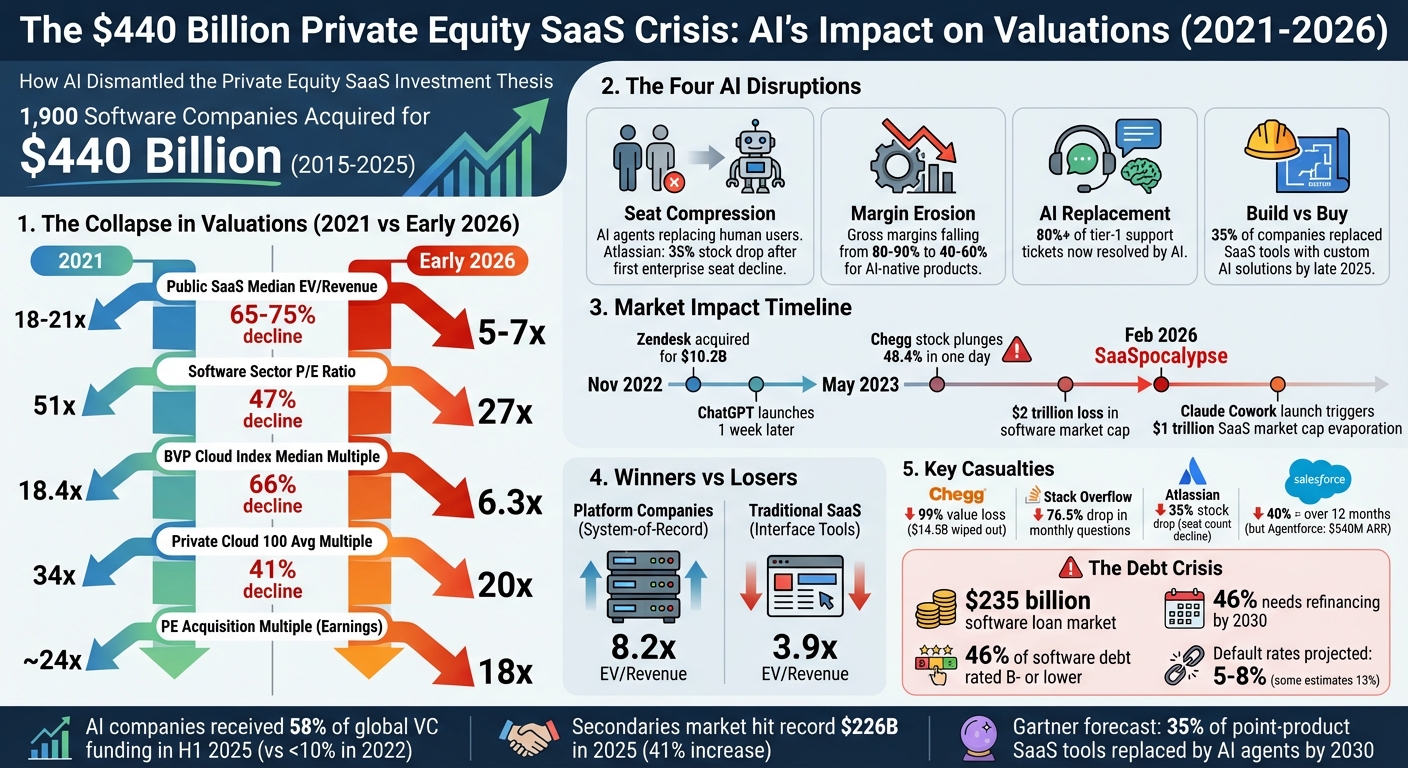

Private equity's $440 billion SaaS bet is unraveling. Between 2015 and 2025, PE firms acquired 1,900 software companies, drawn by predictable revenues, high margins, and scalable growth. But AI is disrupting every assumption behind these deals:

- AI tools are cutting software usage: Fewer licenses are needed as AI replaces human tasks.

- Margins are shrinking: AI's computational costs are slashing profitability.

- Valuations are collapsing: SaaS multiples have dropped 65–75% since 2021.

- Customer behavior is shifting: Businesses are building custom AI solutions instead of buying SaaS tools.

The result? Public SaaS valuations are down, debt-heavy PE-backed companies are struggling, and Wall Street remains silent to avoid triggering panic. AI is not just changing SaaS - it’s forcing a rethink of the entire investment model.

Here’s how the landscape is shifting and what it means for investors, SaaS leaders, and private equity firms.

The $440B Private Equity SaaS Crisis: How AI Disrupted Valuations 2021-2026

The AI Reality Check: Navigating the SaaS CAPEX Trap & Identifying True Infrastructure Winners

The Private Equity SaaS Investment Model: Core Assumptions

Between 2015 and 2025, private equity firms followed a straightforward playbook for SaaS acquisitions: buy businesses with steady recurring revenue, cut costs, boost margins, and sell at higher multiples. This strategy paid off handsomely, generating billions in returns across nearly 2,000 deals [5][2].

The model relied on three key pillars. First, subscription revenue provided stable cash flows, making it easier to secure debt financing for leveraged buyouts. Second, SaaS companies typically enjoyed gross margins of 75% to 90%, with minimal costs for acquiring new customers - an ideal setup for optimizing EBITDA [5][1]. Third, software integrated into essential business functions like payroll or HR created high switching costs, reducing churn and ensuring predictable exits.

"The thesis was elegant in its simplicity: buy a SaaS business with sticky recurring revenues, strip costs, expand margins, and exit at a higher multiple. It worked beautifully."

- Dr. Bhaskar Dasgupta, Chief Mischief Officer [5]

However, AI is now reshaping this model, challenging its underlying assumptions. The speed of disruption has forced private equity firms to reconsider their strategies, from due diligence to exit planning. Let’s break down the revenue, cost, and valuation metrics that formed the backbone of this approach.

Subscription Revenue and Customer Retention Metrics

Subscription-based models offered dependable, recurring cash flows that were largely resistant to economic fluctuations [5]. The real advantage, however, lay in net revenue retention (NRR). Leading SaaS companies often achieved NRR rates above 120%, meaning customers spent more each year through upsells and cross-sells [5][4]. Combined with the stickiness of software embedded in core workflows, this allowed private equity firms to confidently project long-term cash flows. These projections justified high acquisition multiples and significant leverage.

A notable example is the November 2022 acquisition of Zendesk Inc. by Hellman & Friedman and Permira for $10.2 billion. Despite concerns about inflation and a potential recession, the board’s risk assessment didn’t account for AI disruption - this, despite ChatGPT launching just a week after the deal closed [2]. By February 2026, Zendesk had generated over $200 million in annual recurring revenue (ARR) from its AI offerings, accounting for roughly 10% of its total revenue [10][2]. This case underscores both the potential and the risks that AI introduces to private equity investments.

These reliable revenues provided a solid foundation for the aggressive cost-cutting strategies that followed.

EBITDA Optimization and Cost Reduction Focus

Historically, revenue growth drove 53% of private equity value creation, but firms also relied heavily on EBITDA optimization to make their deals profitable [7]. SaaS companies were especially appealing because of their lean operating models. High gross margins and minimal capital expenditures allowed private equity firms to trim costs without compromising product quality.

After an acquisition, firms typically reduced redundant roles and non-core headcount, aiming to boost EBITDA margins from 20–30% to over 40% [3][7].

"We are not a subscriber to any money losing company."

- Orlando Bravo, Founder, Thoma Bravo [7]

But AI is now disrupting this cost-cutting playbook. AI introduces new expenses, such as the costs of compute power and hiring specialized technical talent [8][9]. While traditional SaaS companies enjoyed gross margins of 80–90%, AI-native products are seeing margins drop to 40–60%, as inference costs eat into profitability [1]. AI is also automating tasks that previously required human effort, leading to seat compression - a reduction in the number of software licenses sold - which directly impacts NRR and EBITDA [8][10].

A cautionary tale comes from Navan, which went public in February 2026 with $657 million in debt. Despite a 33% increase in revenue to $537 million, the company posted a $100 million net loss in the first half of 2025, largely due to interest expenses. This resulted in a 60% drop in its IPO price [10]. The case highlights how high debt loads, once manageable with predictable SaaS cash flows, become risky when AI disrupts the business model.

Valuation Multiples by Deal Size and Geography

Valuation multiples for SaaS acquisitions varied based on deal size, geography, and company characteristics. From 2021 to 2024, private equity firms paid an average of 24 times earnings for SaaS acquisitions, with U.S.-based companies and larger deals commanding higher multiples due to perceived lower risk and better exit opportunities.

By 2025, these multiples had dropped significantly. PE-backed SaaS acquisitions averaged 18 times earnings, while broader software EBITDA multiples fell from 30x at the end of 2022 to around 16x by February 2026 [10][5][2]. Revenue multiples declined even more sharply, from 10–12x to roughly 4x over the same period [10].

The drop wasn’t universal. Platforms offering software as infrastructure - those with proprietary data, regulatory advantages, or system-of-record roles - maintained premium valuations of 8.2x EV/Revenue. In contrast, software as interface tools fell to 3.9x [1].

For example, in early 2025, Orlando Bravo led a $12.3 billion acquisition of Dayforce, the largest deal in Thoma Bravo’s history. This was part of a broader $42 billion investment in 2025 aimed at transforming market leaders into AI-powered platforms [7]. Meanwhile, Blackstone’s $16 billion acquisition of AirTrunk in September 2024 - marking the largest private equity deal of Q3 2024 - indicated a shift toward physical AI infrastructure [5][6].

| Metric | 2021 Peak | Early 2026 |

|---|---|---|

| Median Public SaaS EV/Revenue | 18–21x | 5–7x |

| PE Acquisition Multiple (Earnings) | ~24x | 18x |

| Gross Margins | 80–90% | 40–60% (for AI-native) |

| Target EBITDA Margin for PE | ~20–30% | 40%+ |

The data paints a stark picture: the factors that once made SaaS a safe bet for private equity are rapidly changing. AI has accelerated the pace of disruption, forcing firms to rethink their approach in an environment where traditional assumptions no longer hold.

How AI Is Disrupting Traditional SaaS Business Models

AI isn't just improving software; it's reshaping the entire SaaS landscape. Categories of tools that private equity firms poured billions into are being replaced, with AI making waves in workflow automation, content creation, and sales intelligence. These changes are challenging the $440 billion worth of SaaS investments made between 2015 and 2025, fundamentally altering how businesses operate.

In early 2026, the software industry faced a $2 trillion loss in market capitalization during the "SaaSpocalypse" [11]. Public SaaS valuations dropped sharply - 65–75% from their 2021 highs. Median EV/Revenue multiples fell from 18–21x to just 5–7x by early 2026 [1]. This dramatic shift reflects the rise of AI agents, which are turning software from "interfaces" into tools that autonomously complete tasks. As a result, the traditional per-seat pricing model that fueled SaaS growth is being upended.

AI Agents Replacing Manual Workflow Tools

AI agents are taking over tasks that once required human input, replacing tools designed for manual workflows. For example, instead of logging updates or entering customer data, AI agents now handle these tasks on their own, reducing the need for project management and CRM platforms.

In early 2026, Atlassian (TEAM) shares dropped 35% following its first-ever decline in enterprise seat counts. The culprit? AI agents automating task tracking and project management workflows [11]. Tools like Jira and Confluence, which relied on users to manually update tickets and documentation, are now being sidelined as AI agents take over these responsibilities without human intervention.

Customer support platforms are feeling the heat too. AI agents now resolve over 80% of tier-1 support tickets on their own [11], rendering traditional ticketing systems less relevant. In response, Zendesk has adopted a hybrid pricing model, charging per seat for human agents and per resolved ticket for AI agents [14].

"The rise of AI agents that can operate enterprise software autonomously poses a structural threat to per-seat SaaS pricing models."

- Morgan Stanley [12]

CRM platforms are also under pressure. AI agents now log interactions, score leads, and update records automatically, reducing the need for individual user licenses. This "seat compression" is challenging the viability of the per-seat pricing model [14].

| Vulnerability Level | Software Category | Example Legacy Tools | AI Impact Mechanism |

|---|---|---|---|

| High | Project Management | Jira, Asana, Monday.com | Agents handle task tracking autonomously [11] |

| High | Customer Support | Zendesk, Intercom | AI resolves 80%+ of tier-1 tickets; UI becomes redundant [11] |

| High | CRM Data Entry | Salesforce, HubSpot | Agents log interactions and score leads automatically [11] |

| Medium | Business Intelligence | Tableau, Looker | Insights generated directly from raw data [11] |

| Low | Security/Compliance | CrowdStrike, Palo Alto | High error sensitivity protects incumbents [11][1] |

Generative AI Undermining Content and Marketing SaaS

Generative AI has leveled the playing field for content and marketing tools. Tasks that once required specialized software can now be completed with a simple prompt to tools like ChatGPT or Claude. This has driven the cost of creating content to nearly zero, eroding the competitive advantage of traditional SaaS platforms [13].

The market response has been striking. In May 2023, Chegg's stock plunged 48.4% in a single day after management reported that ChatGPT was decimating its homework-help business. By April 2025, Chegg's shares had dropped below $1, wiping out 99% of its market value - a staggering $14.5 billion loss [1][4]. Similarly, Stack Overflow saw a 76.5% drop in monthly questions - from 108,563 in November 2022 to just 25,566 by December 2024 - as developers turned to AI coding assistants [1].

The disruption isn't limited to consumer platforms. Walmart, for instance, saved 4 million developer hours in 2025 by using AI coding tools to automate internal software maintenance and development [1]. Cursor, a tool that capitalized on this trend, reached $1 billion in Annual Recurring Revenue (ARR) by November 2025 with only 300 employees. This translates to a revenue-per-employee ratio of $1.67 million - about four times higher than traditional SaaS companies [1]. Additionally, emerging "vibe coding" tools enable non-technical users to create custom internal solutions, challenging the one-size-fits-all model of legacy SaaS products [1][5].

AI-Powered Analytics Displacing Sales and Lead Generation Tools

AI analytics platforms are redefining sales and lead generation by offering smarter forecasting and decision-making without the need for complex dashboards or manual setup. This evolution shifts value from standalone SaaS tools to AI systems that orchestrate them [14][12].

After Anthropic launched Claude Cowork in February 2026, over $1 trillion in SaaS market capitalization evaporated within weeks [1][12]. The economic impact is clear: AI agents can perform the work of 10 to 15 mid-level employees, drastically reducing the need for per-seat licenses on platforms like Salesforce and HubSpot [14][12]. Top AI-native companies now average $3.48 million in revenue per employee, compared to just $200,000–$400,000 for traditional SaaS firms [12].

Salesforce's journey highlights this transformation. In early 2026, concerns over seat compression led to a 40% drop in its stock price over 12 months. Yet its AI platform, Agentforce, achieved $540 million in ARR by March 2026, growing 330% year-over-year [1][4]. This shift from selling software seats to selling autonomous agent actions underscores the profound changes reshaping the SaaS industry. The predictable revenue models that once justified massive private equity investments are becoming a thing of the past.

Looking ahead, Gartner forecasts that by 2030, 35% of point-product SaaS tools will be replaced by AI agents [1][14].

sbb-itb-9cd970b

Why Wall Street Isn't Talking About the AI Impact on SaaS Valuations

Wall Street is keenly aware of the unsettling numbers. Admitting that AI is unraveling the $440 billion SaaS investment framework could lead to massive write-downs and jeopardize anticipated exit multiples. For instance, in February 2026, Apollo Global Management quietly reduced its direct lending exposure to software from around 20% at the start of 2025 to just 10% by year-end. This move reflects a broader market hesitation as AI challenges the "sticky" revenue model that once defined SaaS success [2].

The stakes are immense. The software loan market, valued at approximately $235 billion, has nearly half of its debt rated at B‑ or lower [15]. Analysts at Morgan Stanley, Keith Weiss and Sanjit Singh, highlighted in early 2026 that 46% of outstanding software debt would need refinancing by 2030, with interest rates hovering around 3.64% [15]. A public acknowledgment of the "SaaSpocalypse" could trigger a credit crisis, leaving struggling software companies as "zombies" - unable to innovate or service their debt.

"The real risk is - is software dead?"

- John Zito, Head of Global Credit, Apollo Global Management [2]

Investor behavior paints a telling picture. While retail investors continue to "buy the dip" on SaaS stocks, corporate insiders are quietly offloading shares. This divergence shows that institutions are eager to exit before the market fully adjusts to the risks AI introduces. Wall Street's silence on the matter underscores how deeply AI has disrupted the SaaS investment model. Nobody wants to be the first to openly acknowledge this shift.

The analysis below dives into these changes, from plummeting valuation multiples to evolving M&A priorities and how private equity firms are being forced to adapt.

The Decline in SaaS Valuation Multiples

SaaS valuation metrics have taken a sharp hit. Over the course of a year, the software sector's P/E ratio dropped from 51x to 27x [1]. Similarly, the BVP Cloud Index's median multiple fell from 18.4x at its peak to just 6.3x by Q1 2025 - a staggering 66% decline [1]. Private markets weren’t spared either, with the Private Cloud 100 average multiple shrinking from 34x to 20x, marking a 41% drop [1].

The market now separates clear winners from losers. Platform companies with system-of-record status are trading at a median of 8.2x EV/Revenue, while traditional SaaS companies hover at just 3.9x - a 2x premium for perceived resilience [1]. For private equity firms that acquired companies at the inflated valuations of 2021, the math is bleak. A company purchased at 15x revenue now trading at 6x represents a 60% loss before any operational improvements. The old strategy of scaling businesses to $20M–$50M in ARR for predictable exits no longer works. Strategic buyers now prioritize AI capabilities, and IPO benchmarks have risen to $400M+ ARR with 30–50% growth [3].

| Metric | 2021 Peak | Early 2026 | Decline |

|---|---|---|---|

| Public SaaS Median EV/Revenue | 18–21x | 5–7x | ~65–75% |

| Software Sector P/E Ratio | 51x | 27x | ~47% |

| BVP Cloud Index Median Multiple | 18.4x | 6.3x | ~66% |

| Private Cloud 100 Avg Multiple | 34x | 20x | ~41% |

AI-Native Companies Changing M&A Activity

The M&A landscape has shifted noticeably. By the first half of 2025, 58% of global VC funding went to AI companies, a massive jump from less than 10% in 2022 [3]. This capital shift has reshaped buyer priorities, with strategic acquirers now seeking AI capabilities over traditional SaaS metrics like seat counts. This trend is reflected in a 24.8% drop in SaaS M&A deal value in early 2025 [3], while AI-native companies are commanding premium valuations. For example, Cursor, an AI coding assistant, saw its valuation skyrocket from $400 million in August 2024 to $29.3 billion by November 2025 [1]. In contrast, traditional SaaS companies are struggling to find buyers at reasonable prices.

The rise of "vibe coding" is accelerating this trend. Tools that enable non-developers to create custom software through natural language programming are fundamentally altering the buy-versus-build equation. By late 2025, 35% of companies had replaced at least one SaaS tool with a custom AI solution [1]. With traditional exit paths narrowing, the secondaries market hit a record $226 billion in 2025 - a 41% increase over 2024 - as limited partners sought liquidity from AI-exposed portfolios [5].

"Technology private equity, in its current form, is dead."

- Isaac Kim, Partner, Lightspeed [2]

As these dynamics unfold, private equity firms must rethink their strategies to survive the AI-driven market transformation.

How Private Equity Firms Must Adjust Their Approach

Private equity firms can’t afford to wait for clarity - they need to act now. First, they must demand higher EBITDA margins (40%+ minimum) and ensure clear AI integration in new acquisitions. Conducting AI vulnerability audits across existing portfolios is essential [3]. Boards need to ask tough questions: Can AI replicate core functions? Are customers building their own alternatives? Is the pricing model still viable in an AI-driven world?

Second, firms must stress-test credit assumptions and shift investments toward sectors less vulnerable to AI disruption, such as healthcare and banking. Default rates in the software sector are projected to rise to 5–8%, with some analysts predicting rates as high as 13% [5][16]. In February 2026, Blackstone’s BCRED fund, which has 26% exposure to software, faced redemption requests amounting to 4.5% of total shares outstanding due to fears of the "SaaSpocalypse" [16]. Healthcare and banking software, with their regulatory safeguards, offer more stability than generic workflow tools. For instance, CVC Capital Partners took over Sabio Group in 2025 after the contact center support business struggled to attract buyers amid AI-related concerns [2][5].

Finally, focus must shift to AI infrastructure. The market is rewarding investments in the backbone of AI - data centers, energy providers, and compute infrastructure - assets that are less prone to obsolescence and have longer lifespans.

"Everyone's focused on these bubble risks. I think the biggest risk is actually the disruption risk. What happens when industries change overnight, like what we saw to the Yellow Pages back in the nineties when the internet came along."

The firms that will endure are not those with the most extensive software portfolios but those that recognize the shifting landscape early. The $440 billion SaaS bet, once seen as untouchable, is being reshaped by AI in ways that demand swift and strategic action.

Conclusion: What Investors and SaaS Leaders Should Do Next

The $440 billion SaaS investment model that defined the last decade is facing a seismic shift. AI isn’t just altering the game - it’s rewriting the entire playbook. In this fast-moving environment, success hinges on how quickly and decisively you act.

Private equity firms should start by conducting AI vulnerability audits within the first 100 days. Assess whether core products can be easily replicated, if customers are developing their own solutions, and whether management is moving beyond surface-level AI adoption. A great example: Vista Equity Partners deployed internal teams to assist its 85+ portfolio companies in integrating AI, leading to a 30% increase in coding productivity. Today, 80% of its majority-owned companies use generative AI tools [5]. Beyond audits, invest in AI infrastructure like data centers and computing resources to establish lasting competitive advantages. Also, focus on regulated industries - banking, healthcare, and insurance - where compliance can slow AI disruption, creating opportunities for strategic investment. These steps will help define how SaaS leaders must rethink their product strategies.

For SaaS leaders, the focus should shift to building deeper, more durable value. Move away from traditional seat-based pricing and adopt usage- or outcome-based models. These models allow you to capture value even as AI reduces workforce needs. Additionally, transition your product from being just an interface to becoming a foundational infrastructure. This means building proprietary data advantages, securing regulatory barriers, and creating "memory moats" - where your product improves with continued use. Take Salesforce as an example: its move to consumption-based AI pricing helped Agentforce achieve $540 million in ARR by February 2026, with 330% year-over-year growth [1]. Profitability is also key - SaaS companies now need EBITDA margins above 40% to meet IPO thresholds, which often require $400 million+ in ARR, 30–50% growth, and solid profitability [17].

For investors, recalibrating benchmarks is essential as portfolio dynamics evolve. Platform companies serving as systems of record are trading at 8.2x EV/Revenue, compared to 3.9x for traditional SaaS [1]. Look for indicators like Net Revenue Retention above 110% and gross margins over 75% - these signal strong customer loyalty. Vertical SaaS, which made up 46% of M&A activity in Q2 2025, offers tighter integration and higher switching costs compared to horizontal solutions [17]. It’s also critical to distinguish between strategic AI - integrated into core intellectual property - and performative AI, which only delivers superficial improvements.

As SaaS valuation multiples continue to decline, these strategic shifts are no longer optional. The question isn’t whether AI will disrupt traditional SaaS models - it’s whether you’ll act fast enough to seize the opportunities it creates.

FAQs

How does AI cause “seat compression” in SaaS?

AI is reshaping the SaaS industry through a phenomenon known as "seat compression." By automating tasks that previously required human input, AI reduces the need for individual users - or "seats" - within a software platform. This shift directly impacts the traditional per-seat pricing model, which has long been a cornerstone of SaaS profitability. As AI continues to take on more responsibilities, it disrupts revenue structures that rely on human-driven software usage.

Why do AI features reduce SaaS gross margins?

AI-driven SaaS platforms are seeing lower gross margins due to the continuous costs associated with AI inference. Expenses like token usage and computational resources are substantial and recurring, which chips away at the traditional near-zero marginal cost advantage of SaaS businesses. As a result, gross margins have dropped to around 40–60%, a noticeable decline from the earlier range of 75–85%. These ongoing costs make it much tougher for SaaS companies to sustain the high profitability levels they once enjoyed.

What should PE firms audit first to gauge AI disruption risk?

PE firms should begin with a thorough audit of their portfolio companies' use of AI. The goal is to assess how well these companies are utilizing AI to maintain or strengthen their competitive position. This evaluation helps ensure they can adapt to and withstand disruptions brought about by AI advancements.