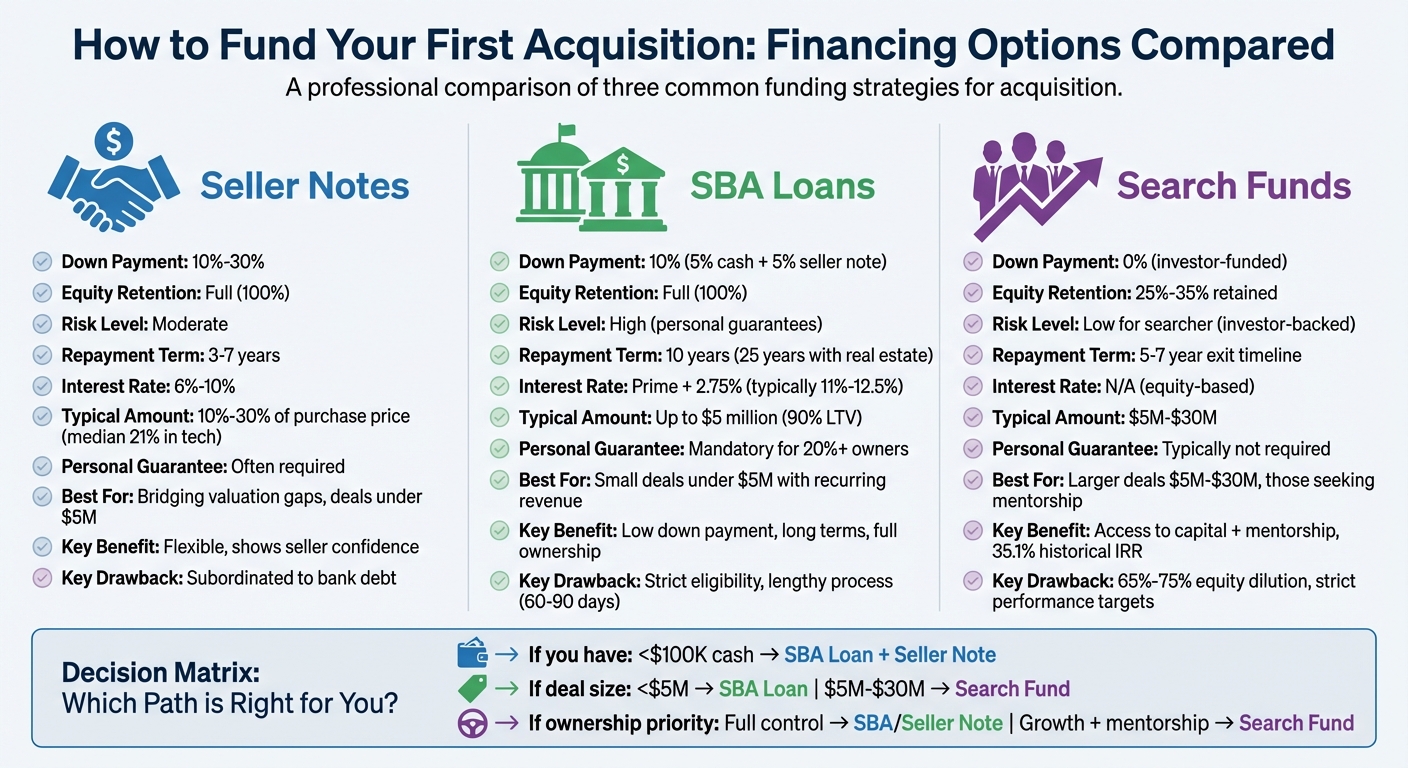

When buying a SaaS or AI business, securing the right financing is critical. Most first-time buyers don’t have the cash upfront, so understanding your funding options can make or break the deal. Here’s a quick overview of three popular methods:

- Seller Notes: The seller finances part of the purchase price, repaid over time with interest (typically 6%-10%). It’s flexible and shows seller confidence but adds debt to your cash flow.

- SBA Loans: Government-backed loans covering up to 90% of the purchase price. They require a 10% down payment (can include a seller note) and personal guarantees but offer long repayment terms (10 years).

- Search Funds: Investors fund your acquisition, but you give up 65%-75% equity. Ideal for larger deals ($5M-$30M) and those seeking mentorship but involves strict performance goals.

Each option has trade-offs in ownership, risk, and deal size. For smaller SaaS buys under $5M, SBA loans combined with seller notes work well. For larger deals, search funds provide capital but reduce your equity stake.

Quick Comparison:

| Feature | Seller Notes | SBA Loans | Search Funds |

|---|---|---|---|

| Down Payment | 10%-30% | 10% (5% cash) | 0% (investor-funded) |

| Equity Retention | Full | Full | 25%-35% retained |

| Risk | Moderate | High (personal guarantees) | Low (investor-backed) |

| Best For | Bridging gaps | Small deals (<$5M) | Larger deals ($5M-$30M) |

Choose based on your cash reserves, deal size, and willingness to share ownership. Let’s dive deeper into how each option works.

Comparison of Seller Notes, SBA Loans, and Search Funds for Business Acquisitions

The Ultimate Guide to SBA Acquisition Financing [Comprehensive 2025]

sbb-itb-9cd970b

Seller Notes: Deferred Payment Financing from the Seller

A seller note allows part of the purchase price to be paid over time, with interest. This setup can help bridge the gap between the buyer's current financial capability and the seller's asking price, especially when traditional lenders won’t finance the full valuation of a SaaS or AI business.

"Seller notes are often the glue that holds the deal together." - HartmannRhodes [10]

This type of financing keeps the seller connected to the business's success even after the sale. A seller agreeing to carry a note often shows confidence in the business’s future. On the other hand, a refusal to offer seller financing might hint at potential concerns. Let’s dive into how seller notes work and why they’re important during acquisitions.

How Seller Notes Work

With a seller note, the seller essentially "loans" a portion of the purchase price - commonly 10% to 30% of the deal’s total value [7][8]. In the tech industry, the median seller note hovers around 21% of the purchase price [11]. This amount is typically repaid over 3 to 7 years, with interest rates ranging from 6% to 10% [6][7].

For example, in February 2026, a manufacturing business sold for $3,200,000. The buyer contributed $160,000 (5%) in cash, the seller provided a $160,000 (5%) note on full standby, and an SBA loan covered $2,880,000 (90%). The entire deal was finalized in just 72 days [9].

When combining an SBA loan with a seller note, there’s a key condition: the seller note must be subordinated. This means the bank gets paid first before the seller receives any payments [7][11]. According to SBA rules updated in July 2025, buyers must contribute at least 5% in cash. However, a seller note on "full standby" (where no payments are made during the SBA loan term) can count toward the remaining 5% of the required 10% equity injection [9]. Understanding these details is essential for comparing seller notes to other financing options.

Pros and Cons of Seller Notes

Seller notes can reduce upfront cash needs, but they come with some trade-offs.

| Pros for Buyers | Cons for Buyers |

|---|---|

| Reduces upfront cash needs, preserving funds for growth and operations [11] | Higher interest costs compared to traditional bank loans [7] |

| Keeps the seller invested in the business’s success during the transition [11] | Monthly debt payments can strain cash flow if growth slows [11] |

| Easier to obtain than bank loans, especially when lenders won’t cover the full valuation [11] | Risk of default - buyers are still obligated to pay even if the business underperforms [7] |

For sellers, the advantages include earning interest on the deferred amount and spreading capital gains taxes over several years through the installment sale method [10][11]. However, sellers also face risks, such as buyer default. Since the note is subordinated to bank debt, sellers might recover nothing if the business fails [7][11].

"A seller note is not free money for the buyer. It is a calculated risk for you [the seller]. Price it, secure it, and negotiate the terms like the loan it actually is." - Livmo [11]

These dynamics highlight when seller notes can be a smart choice, particularly for SaaS and AI acquisitions.

When Seller Notes Work Best for SaaS and AI Acquisitions

Seller notes are especially useful for SaaS and AI businesses with recurring revenue and stable cash flows. These businesses often have high valuations tied to intangible assets like software, customer relationships, and intellectual property - elements that traditional lenders may find difficult to assess. A seller note helps bridge this valuation gap while signaling the seller’s confidence in the business’s future.

This financing method also preserves capital for essential post-acquisition investments, such as marketing, hiring, and product development [11]. For instance, in May 2025, an HVAC business in Northern Colorado with $600,000 in EBITDA sold for $2,000,000. The deal included a $1.5M SBA loan, $250,000 in buyer equity, and a $250,000 performance-based seller note [8].

When a seller is open to carrying a note, it’s a strong indicator of their belief in the business. If a seller refuses any form of seller financing, it’s worth investigating further - particularly in SaaS deals. Seller notes are just one of several financing strategies available to buyers navigating their first acquisition.

SBA Loans: Government-Backed Financing for Acquisitions

The SBA 7(a) loan program is a practical option for first-time buyers looking to acquire businesses with limited upfront capital. Unlike traditional bank loans that often require a 25–30% down payment, SBA loans allow buyers to secure financing with far less cash upfront. With the government guaranteeing 75% to 85% of the loan amount, lenders take on less risk, making it easier to fund asset-light businesses like SaaS and AI companies [13][15].

"The SBA 7(a) loan program is purpose-built for self-funded acquisitions... allowing a buyer to maintain 100% ownership - no investors, no equity dilution."

- Ishan Jetley, Owner, GoSBA Loans [3]

In fiscal year 2025, the SBA backed over $37 billion in 7(a) loans, showcasing the program's reliability and popularity [18]. These loans can cover not just the purchase price (including goodwill) but also additional needs like working capital and AI-specific expenses such as equipment or infrastructure [12][17].

What Are SBA Loans?

SBA 7(a) loans pair private lenders with a federal guarantee, covering 85% of loans under $150,000 and 75% for amounts up to $5 million [12][13][15].

"The 7(a) program is a public-private partnership. The lenders make the credit decisions and lend the money, as with a conventional loan, while the U.S. federal government provides a partial guarantee of the loan to the lender."

- Wikipedia [16]

Repayment terms are typically 10 years for business acquisitions, extending up to 25 years if commercial real estate is part of the deal [13][16]. Interest rates are generally tied to the prime rate, with a spread that usually ranges between 7.25% and 13.25%. Larger loans over $350,000 are often capped at prime + 3% [14][15][16]. This structure helps secure the acquisition while ensuring operational cash flow remains intact. The loans are particularly effective for "asset-light but profitable" businesses with recurring revenue. Buyers generally need a 10% down payment, which can be split into 5% cash and 5% as a seller note on "full standby" - meaning no payments are due during the SBA loan term [13][3][17].

Eligibility Requirements and Application Process

To qualify for an SBA 7(a) loan, the target business must be for-profit, based in the U.S., and meet SBA size standards, which generally means fewer than 500 employees or annual revenue under $7.5 million [12][13]. Certain industries, like gambling, passive real estate investing, and pyramid schemes, are excluded [13][16].

Lenders typically look for a personal credit score of at least 680 to 690, though some may accept scores as low as 640. All individuals owning 20% or more of the acquiring entity must provide a personal guarantee, putting their assets on the line if the business defaults [3][16][17].

"SBA 7(a) loans are fundamentally cash-flow loans - lenders focus more on DSCR and business performance than on fully collateralizing the entire loan amount."

Lenders also evaluate the Debt Service Coverage Ratio (DSCR), which usually needs to fall between 1.15× and 1.25× to ensure the business generates enough cash flow to cover loan payments and owner salaries. While collateral is required if available, the primary emphasis remains on cash flow [14][16].

The application process demands a comprehensive package, including a resume detailing relevant management experience, a business plan outlining post-acquisition strategies, and three years of tax returns for both the buyer and the target business [14][17]. Working with Preferred Lenders (PLP) can expedite the process since they have the authority to make credit decisions without waiting for SBA approval. However, the entire process typically takes 60 to 90 days from start to finish [15][16].

Pros and Cons of SBA Loans

| Pros of SBA 7(a) Loans | Cons of SBA 7(a) Loans |

|---|---|

| Lower down payment (10%) compared to conventional loans (25–30%) | Personal guarantees required for owners with 20%+ stake |

| Longer repayment terms (10–25 years) improve cash flow | Lengthy, document-intensive application process (60–90 days) |

| Capped interest rates prevent excessive costs | Strict eligibility criteria for industries and business size |

| Can finance working capital and closing costs | Collateral required if available |

Guarantee fees usually range from 2% to 3.75% of the guaranteed portion [18]. By allowing buyers to finance up to 90% of the purchase price (when combined with a seller note), SBA loans make acquisitions more accessible for those with limited initial capital.

A great example of the program's potential is Cerner Corporation. This health IT company used a $200,000 SBA 7(a) loan to develop its electronic health records systems. That early funding helped transform Cerner into a global healthcare technology leader worth billions [18]. While this example predates the SaaS boom, it highlights how SBA loans can fuel significant growth in technology-focused businesses.

For SaaS and AI acquisitions, the emphasis on cash flow rather than physical assets makes the SBA 7(a) loan an appealing choice. With large banks approving only about 25% of small business loans, SBA backing significantly boosts approval odds. In fiscal year 2024, 70,242 SBA 7(a) loans were approved, totaling $31.1 billion [16].

Search Funds: Investor-Backed Acquisition Model

When it comes to buying a business, the search fund model flips the script. Instead of finding a business first and then chasing financing, you raise money upfront from investors to fund your search. Once you identify the right company, those same investors - often joined by new ones - supply the capital for the acquisition. In return, you step into the CEO role, while investors take a significant equity share [19][20].

"[It's] the most direct way I know for aspiring MBA entrepreneurs to get into business for themselves."

- H. Irving Grousbeck, Professor, Stanford Graduate School of Business [19]

This model is ideal for individuals with strong operational skills who want to lead a company but lack the personal funds to make it happen. Along the way, investors often act as mentors, guiding you through the process and serving on the board [22].

How Search Funds Work

Search funds operate in three key phases:

- Raising Initial Capital: The first step is to secure $300,000–$700,000 to cover 18–24 months of expenses. This money supports your salary (typically $100,000 to $150,000 annually), travel costs, and due diligence while you search for the perfect business [22][23]. During this phase, you'll evaluate hundreds of potential companies. On average, the search takes 19 months, and roughly 57% of searchers successfully acquire a business [23].

- Acquisition Funding: Once you find a target, your initial investors usually get priority to provide the equity needed to close the deal. New investors often join in as well [21][26]. The typical capital structure includes 30%–40% senior debt (often SBA-backed), 50%–60% investor equity, and 10%–20% seller financing [21]. Early investors are compensated with equity that converts at a 1.5x premium, reflecting the higher risk they took [21][23].

- Operational Management: After acquiring the business, you step in as CEO and focus on scaling it. Your equity vests in three parts: one-third at closing, another third over four to five years, and the final third upon hitting performance targets like a 20%–35% internal rate of return (IRR) [21][23]. This structure aligns your goals with those of the investors while offering substantial upside if you succeed.

While the model offers great potential, it also comes with risks, as highlighted below.

Benefits and Risks of Search Funds

| Benefit | Description | Risk | Description |

|---|---|---|---|

| Access to Capital | Covers both search and acquisition funding [23]. | Equity Dilution | Searchers typically give up 70%–80% of the company to investors [21][23]. |

| Mentorship | Backed by experienced investors who often join the board [22]. | Strict Targets | Performance equity vests only if high IRR thresholds (e.g., 20%+) are met [21]. |

| Lower Risk | Acquiring a profitable business with cash flow is less risky than starting from scratch [20]. | Personal Guarantee | SBA loans may require guarantees, adding financial pressure [3][21]. |

| Path to CEO | A structured route to executive leadership [19]. | Search Failure | If no deal is found within two years, search capital is lost [21]. |

The potential rewards are impressive. Search funds have historically delivered an aggregate pre-tax IRR of 35.1% and a 4.5x return on investment [19][22]. Consider the example of Sandy Paige: at 48, he raised $420,000 in search capital, acquired Explora BioLabs for $2.5 million EBITDA, and sold it four years later for $295 million - a 27–28x return for his investors [23].

"Your equity, or 'carry,' is why you're doing this. But it's not a given - it's earned. While you have massive upside, that equity is worthless unless you successfully grow the business."

- Brett Sleyster, Searcher Insights [21]

Still, the risks are real. About 31% of search fund acquisitions result in losses, and if you fail to find a business within your search window, the fund dissolves, and investors lose their capital [24][25]. Additionally, personal guarantees on SBA loans and the pressure to deliver investor returns within four to 10 years add to the challenge [20][21].

When Search Funds Work Best for SaaS and AI Acquisitions

Search funds are particularly well-suited for SaaS and AI acquisitions. Investors favor businesses with recurring revenue, high gross margins (15%+), and predictable cash flows [20][23]. These qualities make B2B software companies and tech-enabled services prime targets.

Typically, search funds focus on businesses with enterprise values between $5 million and $30 million and EBITDA ranging from $1 million to $5 million [3][23]. For SaaS acquisitions, it's essential to look for companies with diversified revenue streams (no single customer accounting for more than 30%) and strong retention rates that highlight the recurring revenue model investors prefer [23].

Post-acquisition, SaaS and AI buyers have a unique edge. Many use AI tools to streamline operations - documenting processes, analyzing churn, and automating tasks like invoicing. These strategies can significantly boost EBITDA and create value [5].

The key to success lies in having a focused acquisition strategy. Instead of casting a wide net, narrow your search to a few industries where you have expertise. This approach not only speeds up deal-making but also reassures investors of your ability to execute [23]. For SaaS and AI buyers, this alignment with recurring revenue models makes search funds an attractive option.

Comparing Seller Notes, SBA Loans, and Search Funds

When evaluating financing options, it's essential to weigh factors like equity retention, personal risk, and available capital.

Equity retention varies significantly across these methods. Seller notes and SBA loans allow buyers to retain full ownership of the business. In contrast, search funds typically require giving up 65%–75% of equity to investors in exchange for their financial backing and guidance [3].

Personal risk is another critical consideration. Both SBA loans and seller notes require personal guarantees from owners with at least a 20% stake in the business. This means your personal assets - such as your home, savings, and retirement accounts - could be at risk if the business fails. However, seller note guarantees are often subordinated to bank debt. On the other hand, traditional search funds generally don’t require personal guarantees from the searcher, shifting the financial risk to the investors instead [3].

Capital limits also differ across these options. Seller notes typically cover a smaller portion of the purchase price, while SBA 7(a) loans cap at $5 million. Search funds, however, target acquisitions in the $5 million to $30 million range, making them a better fit for larger deals [1][3][8]. These distinctions are particularly relevant for SaaS and AI buyers, helping them align financing choices with deal size and risk tolerance.

Side-by-Side Comparison

| Feature | Seller Notes | SBA 7(a) Loans | Traditional Search Funds |

|---|---|---|---|

| Down Payment | Negotiable (often 10%–30%) | 10% (can include 5% cash and 5% seller note on standby) | 0% (investor funded) |

| Funding Amount | Typically 10%–30% of the purchase price | Up to $5 million | $5 million – $30 million |

| Repayment Term | 3–7 years | 10 years (fully amortizing) | Typically a 5–7 year exit timeline |

| Cost of Capital | Moderate (6%–10% interest) | Moderate (Prime + 2.75%, around 11%–12.5%) | High (with significant equity upside) |

| Equity Dilution | None | None | High (approximately 65%–75% to investors) |

| Flexibility | High (often performance-based) | Low (strict federal guidelines) | Moderate (subject to investor oversight) |

| Personal Guarantee | Often required | Mandatory for 20%+ owners | Typically not required |

| SaaS/AI Fit | Excellent for bridging valuation gaps | Ideal for stable, cash-flowing businesses | Best for larger-scale growth |

This table highlights the key differences, offering a clear snapshot to guide your decision-making process. By understanding these nuances, you'll be better equipped to choose a financing method that supports your acquisition goals and ensures long-term growth.

For SaaS and AI buyers, the choice often boils down to deal size and equity preferences. If you're targeting a smaller business under $5 million with steady cash flow, combining an SBA loan with a seller note can provide strong leverage without sacrificing ownership. However, if you're pursuing a larger acquisition and value the mentorship and resources of investors, a traditional search fund could be the right fit - though it comes with the trade-off of significant equity dilution.

"For most people buying a small business, an SBA loan is practically the only real financing option. Everything else is either a fantasy, a fallback, or a footnote." - Ishan Jetley, Owner, GoSBA Loans [1]

How to Choose the Right Financing Option

Factors to Consider

When deciding on a financing method, focus on four key factors: available cash, deal size, ownership goals, and your personal risk tolerance.

Available cash plays a big role in determining your options. For example, an SBA loan usually requires $75,000–$250,000 in liquid capital to cover the equity injection, search costs, and a post-close financial cushion [5]. Structuring a deal with 5% cash, 5% seller standby note, and 90% SBA loan can reduce your upfront cost to just 5% of the purchase price [3].

Deal size matters too. SBA 7(a) loans typically max out at $5 million, making them ideal for acquisitions between $1 million and $5 million. If you’re looking at businesses valued between $5 million and $30 million, a traditional search fund might be a better fit [3]. For SaaS businesses, lenders often require a Debt Service Coverage Ratio (DSCR) of 1.15×–1.25× [3].

Your ownership goals will also guide your choice. If retaining full ownership is a priority, SBA loans or seller notes are your best options. On the other hand, traditional search funds usually leave you with only 25%–35% equity after investors take their share [3].

Finally, think about your personal risk tolerance. SBA loans come with personal guarantees for anyone owning 20% or more of the business, which means your personal assets could be on the line [3].

Before finalizing your decision, it’s a good idea to consult an SBA-experienced lender to get pre-qualified. For deals over $1.5 million, consider investing in a Quality of Earnings (QoE) report - costing $5,000 to $15,000 - to verify the seller’s financials and avoid surprises during underwriting [5].

With these factors in mind, choose a financing method that aligns with your goals and your comfort level with risk.

Recommendations for SaaS and AI Buyers

Whether you’re buying a SaaS or AI business, your financing strategy should match the specifics of your acquisition.

For smaller SaaS acquisitions under $5 million with steady recurring revenue, consider combining an SBA loan with a seller note. This approach allows you to keep full ownership while using government-backed financing. Look for businesses with at least $250,000–$300,000 in Seller's Discretionary Earnings (SDE) to ensure there’s enough to cover both your salary and debt payments [3].

If you’re targeting high-growth AI businesses, an earnout can help bridge valuation gaps. This structure ties part of the purchase price to future performance milestones, which is especially useful given that AI-driven pricing increases range from 20% to 37%, compared to the typical 3% to 9% for SaaS businesses [2][27]. An earnout helps protect you from overpaying upfront.

For acquisitions over $5 million, traditional search funds can provide the capital and institutional support you need to compete. This route is particularly helpful if you value mentorship and additional resources over complete ownership. However, keep in mind that you’ll likely retain only 25%–35% of the equity, with investors taking the majority stake [3]. Interestingly, self-funded searchers accounted for over 60% of individual acquisitions under $5 million in 2025, showing a strong preference for the control that SBA-backed financing offers [5].

"A 90% LTV loan on a cash-flowing asset is the most asymmetric risk/reward setup available to individual buyers." - Danielle Hunt, EBIT Community [5]

Conclusion

Choosing the right financing method is crucial when navigating acquisitions, especially in the SaaS and AI sectors. Each option offers distinct advantages and trade-offs, so understanding these is essential for making informed decisions.

Seller notes are a great way to bridge valuation gaps and show seller confidence, often covering about 21% of technology deal values [11]. They offer flexibility and can be tied to performance metrics. However, they are subordinated to bank debt and usually require full standby periods [11][8].

SBA loans, on the other hand, provide up to 90% financing with 10-year terms, making them one of the most accessible options for individual buyers [1][4]. They allow you to maintain 100% ownership without external investor involvement. The trade-off? A personal guarantee, which puts your personal assets on the line [28][3].

"For most people buying a small business, an SBA loan is practically the only real financing option. Everything else is either a fantasy, a fallback, or a footnote" [1].

Search funds come in two flavors: self-funded and traditional. Self-funded search funds let you keep full ownership while leveraging SBA loans, often delivering median investor IRRs of 25%–30% with minimal capital loss [3][5][24]. Traditional search funds, suited for larger deals ($5 million to $30 million), bring institutional backing but dilute ownership to around 25%–35% [3][5][24].

Your financing choice depends on factors like available cash, deal size, ownership preferences, and risk appetite. For SaaS and AI acquisitions under $5 million with steady recurring revenue, a structure of 5% cash, 5% seller note, and 90% SBA loan offers high leverage while keeping full ownership intact [3][5]. For larger acquisitions, traditional search funds provide the financial backing to compete, though they come with significant equity dilution.

To set yourself up for success, align your financing strategy with your long-term goals. Work with SBA-experienced lenders early on to secure pre-qualification and ensure your financing aligns with your growth plans [1][5].

FAQs

Can I combine an SBA loan with a seller note?

Yes, it’s possible to combine an SBA loan with a seller note. The SBA permits seller notes on full standby to be included as part of the buyer’s equity injection. This setup can enable financing structures such as a 5% down payment when the seller note is on full standby. This option can make it easier for first-time business buyers to secure funding.

What does a personal guarantee mean for me?

When you offer a personal guarantee, you’re agreeing to be personally liable for a loan if your business is unable to repay it. This means your personal assets - such as savings, real estate, or other valuables - could be used to cover the debt. For SBA loans, owners holding at least 20% ownership are generally required to provide a personal guarantee, making them directly accountable for the repayment.

How do I know if a search fund is worth the equity I give up?

When deciding if a search fund justifies the equity stake, take a close look at its potential returns, the risks involved, and how well it aligns with your personal or financial goals. Think about the advantages it brings to the table - like operational support or specialized industry knowledge. Make sure the equity terms reflect the business's growth potential and profitability. In the end, it's about balancing the benefits against the cost of equity, while keeping your risk tolerance and long-term objectives in mind.